Over the past decade I have become increasingly focused on what I have been calling Central Social Districts (CSDs). The simple analytical framework I’ve been developing saw downtowns being composed of two major components: Central Business Districts (CBDs) and CSDs. However, over the past year or so, email discussions with members of The ADRR board, and an interview by Rob Steuteville at CNU’s Public Square have prompted me to take a much closer look at the vocabulary we use to describe and analyze our downtowns. My objective in this article is to start a discussion of the topic. I don’t claim to have definitive answers, but certainly aspire to getting such a discussion off to a very good start.

In recent months I have again confirmed my conclusion that remote work is here to stay, and that it will undoubtedly impact our large and suburban downtowns. In the past, I felt this was the case because:

So many more employees now have tried and liked remote work. They also have become much better at it

Major corporations are adapting their operations to it and investing substantial sums in equipment and programming to help assure its optimal performance. This is even happening in major companies whose CEOs were initially opposed to remote work

There is much wider acceptance of remote work. Importantly, those who engage in it are far less likely to be seen as slackers or second-class employees.

Recently, I have also come to see the critical importance of remote working being a response to needs other than those related to the pandemic. This is critically important because new or heightened trends will only persist past the crisis that impacts them if non-crisis related needs are there to sustain substantial future interest in them. That critical non-crisis related need for remote work, I would argue, is related to the “unbonding” of creatives working for corporations. Just as there are forces that bond together atoms, ions, or molecules to form chemical compounds, so there are forces that make creative employees bond or unbond to the companies that employ them. The pandemic has reinforced those that press toward unbonding. This unbonding may not mean the termination of the relationship between creative employees and their employers. However, it certainly does mean a change in it, and a loosening of the bonds between them so that the workers have much more control over their work and personal lives. Remote work allows the workers to have greater control while still maintaining a meaningful relationship with their employers. In turn, remote work allows employers to retain and attract desperately needed highly talented employees.

It increasingly looks like remote work will have serious negative impacts on our large office dependent downtowns, and potential positive impacts for many suburban and some rural regional commercial centers, i.e., those at the center of small metro areas. The time has come in the downtown revitalization field to look more seriously about how the negative impacts of remote work in our major downtowns can be offset, and how its positive impacts in the suburban and rural areas can best be leveraged.

As the readers of this blog probably know, I have spent a lot of time and effort on identifying the components of our Central Social Districts and analyzing what makes them succeed or fail. I’ve dug deeply into public spaces, movie theaters, housing, and various other components in cities large and small.

Recently, I was asked for one article that put it all together. I realized that I did not have one, so I consequently set out to write it. That article was recently published in The American Downtown Revitalization Review – The ADRR at https://theadrr.com/

Doing the topic justice meant that it would be long, about 30 pages, and more like a monograph than an article. Readers wanting a quicker take can just focus on the first six pages. However, if you are looking for more guidance about what to do and not do, you will need to dig deeper into the article.

Some of the important things I tried to do are to establish that some components are much easier and cheaper to establish than others, and which work better in different types of downtowns. I also tried to strip away a lot of the advocacy hype about some components that too often hides the challenges involved and obscures how progress needs to be evaluated, e.g., the arts venues, while spotlighting venues whose importance still goes widely unrecognized, e.g., libraries.

Here’s the article’s tease and link:

Strong Central Social Districts: The Keys to Vibrant Downtowns

By N. David Milder

DANTH, Inc.

CSDs and Some of Their Frequent Components. Since antiquity, successful communities have had vibrant central meeting places that bring residents together and facilitate their interactions, such as the Greek agoras and the Roman forums. Our downtowns long have had venues that performed these central meeting place functions, e.g., restaurants, bars, churches, parks and public spaces, museums, theaters, arenas, stadiums, multi-unit housing, etc. The public’s reaction to the social distancing sparked by the Covid19 pandemic, and the closure of so many CSD venues, was a natural experiment that demonstrated how much the public needs and wants these venues. They are the types of venues and functions that make our downtowns vibrant, popular and successful. To read more click here : https://theadrr.com/wp-content/uploads/2021/07/Strong-Central-Socia-LDistricts-__-the-Keys-to-Vibrant-Downtowns__-Part-1-FINAL.pdf

Back in 2018, I posted an article with that title to my Downtown Curmudgeon blog. In retrospect, I think it did a fairly decent job of explaining why, though tourism can certainly be very helpful, it is not always a desirable strategic path for economic growth and community well-being. Recently, events such the public disorder caused by spring break tourists have also signaled that not all types of tourism might mesh with a host community’s needs and wants.

Also, there can simply be just too many tourists, and they can threaten to kill the goose that lays the golden eggs. Sometimes it’s their sheer numbers, other times it is also their behaviors. For example, these days local officials in Europe:

“…want to redirect the streams of tourists, as officials in Rome are trying to do, or even to limit them, as Dubrovnik is doing. Barcelona is no longer approving new hotels, Paris has strictly regulated Airbnb and other apartment rental platforms….” Der Spiegel staff. “Paradise Lost: How Tourists Are Destroying the Places They Love.” Spiegel Online.

In response to the stresses and damages tourism can cause, the concept of sustainable tourism emerged around 1990. Initially it focused on ecological issues at scenic places, but in recent years it has been expanded to also look at a location’s socio-cultural charteristics. For example, for one business consultant in Asheville, NC, sustainable tourism means: .”… making a low impact on the environment and the local culture while generating future employment for local people and ensuring a positive experience for locals and tourists alike.” See Max Hunt, Making local tourism sustainable, April 23, 2016.

Back in 2004, a plan for sustainable tourism prepared for the Downeast region of Maine noted that: “ We know that the vibrancy of such an industry (tourism) depends on the quality of the natural and cultural experiences offered. We also know that Downeast Maine has an abundance of such experiences and resources. However, tourism can be a destructive force when not properly planned or managed.” (See: Down East Sustainable Tourism Initiative Year 2010)

Implicit in this notion of sustainability is that tourism needs, in some way, to be properly managed. This, of course, carries along with it the potential for a lot of political opposition.

In my Boom or Bane article, I also noted that “…too may downtown and Main Street leaders leap at a tourist growth strategy without properly thinking through its possible drawbacks as well as its advantages.” The objective of this article is to try to stimulate and facilitate such thinking. Considering how tourism can be properly managed to make it sustainable should be an essential part of that thinking. To my ken, while here in the USA some smaller communities and scenic regions have adopted sustainable tourism plans, tourism leaders in our larger cities and downtowns have not yet picked up on the need for sustainable tourism. Perhaps it is time they did.

TYPES OF TOURISM

Some good starting points for understanding tourism’s complexity are that:

There are many different types of tourism

Towns and downtowns can have combinations of them

Some may have inherent conflicts with others

They each may vary in the way they reward or harm local business and residents

Rather than vaingloriously trying to present a definitive typology of tourism, some examples of the different types will be offered here to demonstrate their existence.

Tourism Defined by Type of Stay. Vacation homeowners (e.g., Palm Beach, the Berkshires, the Hamptons), multi-night visitors (e.g., Los Vegas, Santa Fe, New Orleans, NYC, Paris), and day trippers (e.g., Coney Island, and Belmont’s “Little Italy” in The Bronx) can create distinct types of tourism that reflect their differing incomes and spending patterns, knowledge and concern about the community, and incentives for orderly behaviors. Their impacts on local retailers and service providers are also likely to vary. All will need restaurants, but to varying degrees. Homeowners and day trippers will not need hotels. Some vacation homeowners will spend considerable parts of a year in these homes and come closer to having a range of retail and personal service needs similar to those of local residents than the overnighters or day trippers, but others will hardly ever be at one vacation home because they have so many. Those that do spend time in one location also are far more likely to be concerned about protecting the social and physical aspects of their vacation community, and to know about and be susceptible to local social and legal pressures to maintain local norms and values than the overnighters or day trippers.

In contrast, as a recent report from Key West demonstrates, lots of day trippers – in this instance from cruise ships – can have strongly adverse impacts on a downtown: “On streets where art galleries, fine restaurants and specialty shops once flourished, vendors hawk bawdy T-shirts and stores advertise ‘Everything inside $5.’” In Woodstock NY, town officials shut the popular Big Deep and Little Deep swimming holes because of the “littering and messes left behind by outside visitors.”

Defined by Type of Arrival/Departure. This is a subset of day tripper tourism. Some day trippers will travel to a location alone or in small groups, and they usually are easily absorbed into the places they are visiting. However, others arrive in a bus, or a group of buses, or a cruise ship, or a group of cruise ships. The infusion of the larger groups can mean the sudden entry of hundreds or thousands of tourists into a relatively small area. In such areas, such as downtown Key West, downtown Hamilton in Bermuda, or Piazza San Marco in Venice they can flood the place with people in a way that changes how they normally operate, and consequently robs them of much of the charm that made them attractive and famous.

Defined by Type of Activity Sought. Most local flows of tourists probably are based on the opportunities offered in a location to engage in various types of activities, and the experiences they offer:

To visit scenic sites likes the Grand Canyon or Niagara Falls

To engage heavily in some type of athletic or cultural activity such as to go skiing in Aspen or Killington, or play golf at Pinehurst, NC, or St Andrews in Scotland, or see Broadway shows or visit museums in NYC, or to enjoy the beaches along Florida’s long coastline

To do business – in many large CBDs this can be the largest source of tourists

To gamble, e.g., in Las Vegas or Monaco

To have sex : e.g., in “red light districts” such as: De Wallen in Amsterdam; Soi Cowboy in Bangkok; Frankfurt, Germany; Montmartre – Paris; Hamburg, Germany; Villa Tinto – Antwerp; Broadway – San Francisco

To legally buy and use drugs. Coffeehouses in Amsterdam can sell pot that can be consumed on the premises. It should be noted that the legalizations of various vices, e.g., drugs, and prostitution, are motivated by needs to get them under control. Gambling is more often motivated to raise government revenues.

To party with groups of people. This might occur in a wide variety of indoor places such as hotel rooms, restaurants, night clubs and bars, but also in many public areas such as sidewalks, streets, parks and beaches. Since partying often means consuming large amounts of alcoholic beverages and/or drugs, when it occurs in public places there is a strong built in probability that some level of public disorderly conduct will occur. Problems, such as the recent riots in Miami Beach, or those in Palm Springs back in 1986, or in Daytona Beach in 1955, or in Seattle in 2003, or Columbus, OH also in 2003 can occur when the levels of partiers and disorderly conduct get too high in public spaces.

Defined by Expectations of Behaviors. How a town promotes tourism by signaling the types of behaviors it permits and/or values can have a big impact on the type of tourist it attracts, and how they will behave. It is no surprise that the tag line used to market Las Vegas, “what happens in Vegas, stays in Vegas,” was so successful. Nor is it surprising that the bon mots for promoting New Orleans are “let the good times roll.” Both overtly suggest that at least a little bit of naughtiness mixed with uninhibited festivity can be found by visitors in their cities. This theme then can become a key element of not only the image the tourism promoters are projecting, but also a crucial component in their city’s or downtown’s functional local culture.

However, the theme of naughtiness and uninhibited festivity can also meaningfully be projected by the types of behaviors visibly tolerated within a district such as:

Littering and public urination

Public drinking and drug use

Public drunken or drugged disorderly conduct

Sidewalks, street beds, and public spaces taken over by disorderly people.

While projecting such a covert image may indeed attract tourists for whom partying is a high priority activity, it conversely can make many local residents and workers, and potential tourists see the area as too disorderly and fear engendering to visit. For example, such disorderly behavior by spring break tourists in Palm Springs in 1986 provoked strong complaints by local residents that led to municipal leaders working against attracting spring break tourists.

SOME DIAGNOSTIC QUESTIONS

Answering the following questions can help local leaders to get on the path of creating and maintaining a sustainable local tourist industry.

Will//are the positive benefits of tourism be/being widely shared by residents and town businesses, while negative benefits will be/are small, adversely impacting very few residents and businesses?

Way back in 1936, the political scientist Harold Lasswell postulated that to properly understand politics it’s extremely helpful to ask the basic question: who gets what, when and how? Its application to tourism-based economic development strategies and programs also can be very revealing. We can expect that the answers to this question will vary depending on the type or types of tourism being considered or already implemented, and the socio-economic-cultural conditions in each specific town or downtown. Answering the what, when, and how question should provide a lot of good, evidenced-based insights into which parts of the local tourist industry needs management to become sustainable.

The What. If tied to the understanding that the “what” includes other things than the variables generally used in input-output model impact assessments – e.g., increased number of jobs, and revenues of local households and businesses — then answering Lasswell’s questions can greatly facilitate a proper assessment of the impacts of an existing or proposed tourism program or strategy, and its true value to the community.

The Use of I-O Models. Most of the established types of impacts that tourism can have on a community are beyond the variables and explanatory vocabulary that input-output models are confined to. For example, tourism can:

Increase jobs, but they can be low-paying or decent paying, sustainable or unsustainable. More on this below.

Produce more business opportunities, but also lead local businesses to favor tourist patrons over those who are local residents

Create more interesting shops and entertainments, but also higher retail and restaurant prices

Heighten demand for local housing and commercial properties, but also produce significantly higher prices for both, Affordable rental housing, even for those with relatively substantial incomes has become a serious issue in our downtowns, especially in our largest cities. A study in 2014 found that:” On average, more than half (52 percent) of all rental households spend more than 30 percent of income on housing in the top 25 cities.” SOURCE: Governing calculations of 2014 U.S. Census Bureau American Community Survey data (Table B25070 in “Family Housing Affordability in U.S. Cities, Governing, November 2015). In some cities, like Miami Beach, much needed affordable units are be changed into Airbnb and short-term rental uses. And to repeat: Barcelona is no longer approving new hotels, while Paris has strictly regulated Airbnb and other apartment rental platforms

Increase local tax revenues, but also increase the need for municipal services such as sanitation, police and fire — and the costs of providing them

Create a loss of the community’s character. For example, during the pandemic, concern about this has emerged in the core of Amsterdam among local residents, Its red light district and coffeehouses selling pot, and its streets jammed with foreign tourists has made local residents wonder whose city it is, and what is still left for them to enjoy. Similar concerns have also arisen in many other European cities such as Barcelona and Venice. It also has happened in many relatively small charming towns here in the USA where so many tourists flock to visit that their numbers and behaviors threaten the very charteristics of the place that made it an attractive tourist destination. For example, in Peterborough, NH, the population has a very strong self and town identity. An assessment of its tourism found that for residents “a main priority was maintaining a town for the comfort of the local population and not for tourists.“ Peterborough’s charming and preserved “New England atmosphere,” its history and old buildings, its well-known artists’ colony, the Lowell Colony, are major attractions for tourists.(See: Tomoko Tsundoda and Samuel Mendlinger, “Economic and Social Impact of Tourism on a Small Town: Peterborough New Hampshire.” J. Service Science & Management, 2009, 2: 61-70 Published Online June 2009 in SciRes) These are quality of life (QoL) type concerns, not about increasing the wealth of the locality, or how that increase is distributed.

Increase traffic and poor air quality; these are also QoL type concerns

Generate significantly more crimes associated with public disorder, such as public prankstering, littering, public urination, public drinking and drug use, vandalism, and rioting. This, too, is a QoL concern. One thing we know from the history of our downtowns is that public disorder and heightened public fears can have severe negative impacts on local businesses, property values, and a district’s image.

Too many tourists can severely diminish a downtown’s walkability, thereby making pedestrian activity far less enjoyable, and seriously wounding the district’s image as a desirable place to be. See: Nicole Gelinas. “Planet Travel. Globalization has created a tourist boom in world cities—but masses of tourists create new challenges.” City Journal. August 31, 2018,

This analytical tool also is usually inappropriate for assessing tourism’s impact on a town or downtown because their geographies are far too small for an I-O model to be properly utilized.

Downtown leaders need to realize that some of their tourism attractions may have much more favorable impacts on some dimensions at the county or regional level than on their smaller localities. The expenditures of local theater or performing arts center, for example, can account for about half of its economic impacts on employment, and business and household revenues, but most of those jobs and revenues may well go to people and businesses located outside of the theater’s town or downtown. However, their impacts on real estate may be very local. See ND Milder, “The Impacts of Arts Events Venues on Small Downtowns,” Economic Development Journal 17 (4), 37.

The known potential impacts listed above suggests that the “whats” that people and businesses in a locality can get from tourism can be positive or negative, and in many instances they can be conflicting.

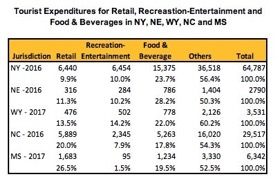

Tourism as an Engine for Retail Growth. My observations, and interactions with potential clients over several decades, strongly suggest that tourism is very often seen as a potential key engine for retail growth in the revitalization strategies prepared for our downtowns. This point consequently deserves some special attention. In all too many instances, especially where the strategic focus is on gambling based tourism, it even has been seen as the growth engine for the whole local economy. Atlantic City and the new casinos in the Catskills in NY are good examples of this. This is especially true for those that are smaller and medium sized communities, and most likely to be hindered by trade areas with low spending potentials. However, in many states – see table above – retail only accounts for around 10% to 15% of tourist expenditures, and when the percentage is higher, the actual expenditure amounts, as in MS, are still often relatively low, or the expenditures for recreation and entertainment are low, as in MS and NC, so the retail percentage becomes de facto higher.

While tourism so often seems attractive as a retail growth strategy, a strong argument can be made that downtowns that already have a robust retail presence are much better positioned to attract tourist shoppers. This hypothesis is supported by the high levels of tourist retail sales that can be reached in our larger downtowns with famed retail districts such as Madison Ave and Fifth Ave in NYC, Rodeo Drive in L.A., North Michigan Avenue in Chicago, and Newberry Street in Boston. For example, a 2018 report on the impact of tourism in NYC found that:

“Tourists account for 18 percent of all Visa transactions at retail stores in the city. They account for an even higher share of sales at the department stores (48 percent), electronic stores (35 percent), and sporting goods stores (23 percent).”

Of course, those high levels of tourist sales are also probably strongly influenced by the incredibly high number of tourists that visited the city pre-pandemic. According to NYC & Co’s annual report: “In 2019, NYC tourism hit a record high—66.6 million individual trips, with about $47.4 billion generated in direct spending for the city ….”

NYC and several other major downtowns also attract large numbers of foreign tourists who tend to spend significantly more in retail shops than domestic tourists.

As the recent pandemic has shown, downtown retail that is heavily dependent on tourist dollars is more susceptible to the negative impacts of substantially decreased tourist flows – particularly form abroad – resulting from severe economic recessions, natural disasters, and diseases.

Contrary to many situations where tourism may seem tempting as a potential retail growth engine, it is unlikely to be a viable, productive strategy in downtowns where the existing retail is weak, and the current tourist traffic is negligible. Such districts have no product to sell, and no market to sell to. The best way out of this situation is to first build an attractive array of retailers that are focused on local customers and products – then, there may be a potential for attracting new tourist retail customers. Also, tourism is then best strategically positioned as an additional source of some retail revenues, but not as the primary source.

Tourism as an Engine for Job Growth. Job growth is an important metric in the economic development field, especially when it comes to justifying investments in new programs and projects aimed at stimulating or implementing growth. Tourism’s ability to produce jobs, however, is rather complicated, and worthy of a closer look.

The strongest argument I’ve seen for tourism being a strong engine not only for job growth, but also for fairly good jobs came in a report by the Center for an Urban Future, that claimed NYC in 2018 had:

“ …nearly as many accommodations jobs, which pay $62,000 per year on average, as jobs in manufacturing, which pay an average of $58,000. To be sure, many of the jobs in the sector offer relatively low wages, at least to start. But tens of thousands of tourism positions provide critical entry points into the labor force for a highly diverse range of New Yorkers. Indeed, no other sector offers as many accessible jobs, with 91 percent of tourism jobs open to workers with less than a bachelor’s degree.” It also claimed that tourism was driving NYC’s economic future. See: “DESTINATION NEW YORK: Spurred by 30 million more tourists over the past two decades, tourism is now driving NYC’s economic future.” May 2018, p.3.

The claim that “tourism is now driving NYC’s economic future” was startling. That the average pay in the industry now was better than that in NYC’s manufacturing industries and at $62,000/yr was very impressive. The claim that no other industry offers as many accessible jobs to those without a college degree was also credible and noteworthy.

I then had a quibble about the use of average incomes since in an industry such as tourism, the difference between its median and average salaries could be significant, and the median could tell us more about how many of those workers had relatively low salaries. Still, the median household income in NYC in 2018 was $63,799, the average was $67,844. The average salaries in NYC’s tourism industry were only about 9% lower than the city average household income, suggesting they may be providing close to a survivable income.

But Covid19 drastically changed things in 2020, especially in NYC. It hit very hard the jobs in the food and lodging industries, with 250,000 of them disappearing, over half of those that existed at the start of 2020. Similar losses occurred all across the nation, wherever the pandemic wreaked economic decline. And this points to some of the built-in vulnerabilities of a tourism job growth engine:

Tourist employment is very susceptible to economic downturns caused by depressions and recessions, natural disasters, and disease

According to BLS : The industry with the highest percentage of workers earning hourly wages at or below the federal minimum wage was leisure and hospitality (11 percent). About three-fifths of all workers paid at or below the federal minimum wage were employed in this industry, almost entirely in restaurants and other food services. For many of these workers, tips may supplement the hourly wages received. A large portion of the jobs associated with tourism just do not pay that well.

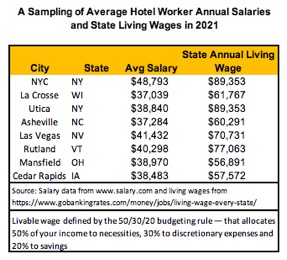

A closer look at the occupations associated with tourism, such as hotel employees, shows they do not have high salaries, e.g., in the sample of eight cities listed in the table above the median is only $38,970, with a low of $37,038 and a high of $48,793. Importantly, none come close to providing by themselves a livable wage.

While in our major cities with robust tourist industries such as NYC, Washington DC, LA, and NYC there are peaks and ebbs in the flow of visitors, a significant flow is usually maintained year round, so employment has some stability. In smaller towns and cities, especially if the tourists are attracted to activity opportunities that are weather dependent, such as skiing and water sports, the tourist flows are seasonal, and so is the employment.

Provincetown, MA, is a good example of such seasonality. It has a population under 3,000 year round, but can have 65,000 people visiting its galleries, restaurants, and beaches. “But come late fall, the beaches and bars mostly empty out. And it is not just tourists who decamp. Most second-home owners pack up, too. And, increasingly, so do people who once made Provincetown their home year-round. These days, just 2,800 hardy souls endure here through the winter. As a result — with housing and year-round jobs increasingly scarce — Provincetown is hollowing out. The winter population dropped 14 percent between 2000 and 2010. Families have left or have avoided settling here in the first place. The high school closed a few years ago.” See: Katharine Q. Seelye, “Welcome to Provincetown. Winter Population: Dwindling.” NYTimes. Dec. 20, 2015.

Similar seasonality is found in Greenport, NY. It is located on the North Fork at the eastern end of Long Island, and has a significant waterfront with docking facilities for pleasure boats, a small fishing fleet and a ferry to Shelter Island, and a waterfront park that attracts over 300,000 visitors a year.. It also has the terminus for an important line of the Long Island Railroad. Within easy drives of the village are over 40 wineries that attract heavy tourist traffic to their tasting rooms. There are three of historical sites abutting or near the park including a working blacksmith shop and a maritime museum. It is a significant tourist destination and transit point. For example, an annual three-day Maritime Festival reportedly draws about 40,000 visitors and the less frequent, multi-day Tall Ships events can attract over 60,000. However, it only has a year round residential population of 2,200,and many of the shops, sometimes even including the local supermarket, close for the winter. Of course, their jobs go dormant, too.

Is the town primarily concerned about how tourism can improve its quality of life or in maximizing the wealth of its residents and businesses?

This question is meant to flesh out a community’s growth values that too often really have not been clarified or adequately discussed in public. However, if tourism is to be beneficially managed, clarity about these values must be achieved.

Of course, QoL and wealth are closely related topics, and some might argue that at the community level, wealth should be grown so that it can support a better QoL. My field observations, however, strongly suggest that when tourism’s objective is only seen as growing the community’s wealth, then it is far more likely to take on characteristics that make it more unsustainable, and more likely to conflict with the type of QoL that local residents have or are striving for.

Sure, at the real estate project level, tourist projects will regularly need to undergo an environmental review, but those reviews are often unlikely to cover some important issues that might be disturbing to current and potential local residents, such as the attraction of tourists who have a high probability of behaving in a disorderly manner, or the loss of community identity.

Also, when a town’s tourism’s primary objective is growing wealth, the project permission’s and approvals process is more likely to adhere to the “bigger is better” adage, as well as “the more expensive a project is, the better it is” rule.

When wealth maximization is the ruling norm, then the town is more unlikely to have or to create a local tourist industry that is sustainable.

The Over-Tourism Question: Are there instances where there are just too many tourists in the town, and their presence is changing in undesirable ways the appearance of the community/downtown, its character, or how these places work?

As noted above, this is the question that is being asked by municipal leaders all over Europe, who are concerned about the strong negative impacts that simply having too many people in a relatively small public space can have. Even the Vatican is concerned about the severe overcrowding by the 6 million visitors annually to its museums – see photo below.

Here in the USA, concerns about over-tourism among downtown leaders has not so far emerged. This is probably due to their being correctly trained to believe that downtowns are successful, full of vibrancy and shoppers when there are high levels of pedestrian traffic. For instance, the managers of Times Square proudly publicize that: “Nearly 360,000 pedestrians enter the heart of Times Square each day. On the busiest days, Times Square has pedestrian counts as high as 450,000.” Those pedestrian flows are equal to the entire populations of the 44th and 55th largest cities in the USA! In one day!

With most with things in our lives, there is a threshold above which a situation is deemed too much, and undesirable. Too much champagne, and one gets drunk. Too much chocolate, and one gets fat. Too many people in a boat, and it might sink, and people may drown. Drive at 150 MPH and one might have a tragic accident. But downtown leaders here in the USA do not seem to have found any pedestrian or visitor count that is too much because of their ill effects. Might 360,000 to 450,000 people trapsing through a relatively small urban area be too many? Or 15,000 passing by one corner in an hour?

The same thing can be said about many of our major tourist attractions, and particularly here in NYC, where being “world class” is a mantle many seek and proudly proclaim. Prior to the pandemic, for example, The Metropolitan Museum of Art had over 6.5 million visitors annually, and MoMA had over 2.2 million. And at both museums, tourists accounted for 75% of their visitors. The net result at these museums are overly crowded galleries, much like rush hour subway cars, where it is habitually hard to see the art either from the distance one would like or for the length of time one would prefer. This unpleasantness is compounded by the too frequent jostlings from other guests, and the annoying behaviors of people from other cultures, be they domestic or foreign. Also unpleasant are the nasty world class lines to get into too often badly maintained restrooms, or to check and retrieve your coat. Nevertheless, the managers of these museums show by their lack of appropriate action no interest in improving the visitors’ art appreciation experience, yet they yearn for even larger attendance that they can brag about. Their building expansions are like adding more lanes to our highways –they just increase the amount of space that will be filled with overly dense visitation.

Similarly, about 66% of the eight million tickets sold annually pre pandemic for Broadway shows went to tourists, and mainly to those who could afford relatively high prices. So, while these museums and Broadway shows are world class, their overwhelmingly dominant use by tourists leaves many NYC city residents feeling that these parts of the city are no longer theirs, but taken over by those “from afar.” Some question whether these residents have a right to this sense of psychological possession and identification, while others, such as Jane Jacobs, might argue that such a sense makes for strong communities.

Public Disorder Question 1. Do tourists primarily want to party, or to look, listen, taste and touch to appreciate the town’s non-party assets?

During the 1970s and 1980s, public disorder and the fear of becoming a crime victim were very strong factors in the steep declines of our downtowns. As I have recently written, the problem of disorder now is resurging across the nation and in a perhaps even more powerful form, since it is much more multifaceted. Consequently, the types of tourism that are highly likely to cause problems of public disorder need to be looked at very closely.

Where large numbers of tourists are intent on partying in public, problems of disorderly conduct are very likely. That can be very offputting to local residents as well as to other tourists who are not as intent on partying. Lots of parting tourists also means high municipal spending for public safety services than would otherwise be needed.

Naughty Los Vegas is an isolated counter example. It’s residential growth was based on the tourism growth generated by its gambling, live and let live social mores, and reputation of mob involvement. New residents knew the type of town they were moving to.

What downtown experts have learned and taught for decades is that how the people act and look when walking on a district’s sidewalks, or in its public spaces, or going in and out of its buildings has an enormous influence on the image the public at large holds of that downtown. It not only sets up expectations in the minds of observers about how people in these places will behave – as do the related signs of disorder discussed by George Kelling and James Wilson, and Wesley Skogan – but also signals how the observers themselves probably would be allowed to behave in that locality.

In some instances, otherwise seemingly harmless behaviors can be disorderly, but then creep into more serious criminal behaviors. In 1986, for example, Palm Springs had its most serious spring break student riot, after which town leaders decided on an anti spring beak policy. But the riot started off with the simple, prankster-like use of squirt guns, that then quickly escalated to dumping water balloons into expensive convertibles, and tearing off the tops of bikini’s worn by women in cars. Cruising rioters also blocked major roadways.

In other instances, as in Miami beach these days, toys such as slingshots, jet skis and e-scooters can become nuisances that require regulation.

Public Disorder Question 2. Does or will the town’s marketing feature the community’s scenic, social and cultural assets or how easy it is for tourists to party in the town?

The objective of this question is to clarify and make public some of the impacts the town’s tourist marketing is having on some of its QoL problems. This might lead to a change in the marketing, or it might spark more effective mitigation programs, such as more police who are well trained to deal with public disorder issues, or new ordinances that regulate the behaviors allowed in public places. For example, one might argue towns that market themselves as great places “to party,” and then have partiers riot, in a real sense, have been asking for it.

Public Disorder Question 3. Are the town’s laws, and their enforcement, that govern its public spaces and sidewalks tolerant of public drinking, drug use and sale, and other forms disorderly conduct or intolerant of such behaviors?

These practices can have a big impact. It is important that town and/or downtown leaders be cognizant of them so they can be changed and improved.

They were used effectively in Palm Springs: “In the years after the riot, city leaders and police would intentionally sabotage spring break with irksome laws intended to chase away college-age tourists.” They banned thong bikinis, throwing water balloons, and shooting squirt guns. Poolside drinking was limited, and “a special $15 fee that was added to all police citations, but only during the 10 days of spring break.” At spring break time, over 200 concrete barricades intentionally created a downtown traffic jam designed to frustrate spring break cruisers.

Sometimes, the solutions are less punitive in character. For example, lots of people walking in the street beds and congesting traffic is a sign of disorder. But if the sidewalks are narrow and or being used by outdoor dining or retailing, then enlarging the sidewalks can be a very viable solution. Another could be providing well activated public spaces where these street pedestrians can engage in enjoyable and socially productive activities, such as those available in Bryant Park.

Is the town committed to making its tourism sustainable, and have the appropriate policies, programs, and regulatory tools needed to manage it? If not, can it create a sustainable tourism program?

Sustainable tourism does not appear organically, though the unsustainable version seems to be able to do so. It requires intention, leadership, resources, knowledge, political support, and strong coalition building. It will likely have many well placed and influential opponents, most likely including those who own or otherwise are benefiting from the unsustainable tourism assets.

If the campaign for sustainable tourism poses its benefits largely in terms of public goods like clean air and water, and general quality of life, that everyone can enjoy, and for which the needs are not that immediate, it will likely languish. People will likely take a free ride and let others try to make it happen. (See: Mancur Olson. The Logic of Collective Action: Public Goods and the Theory of Groups. Harvard University Press, 1971). To build a winning coalition within the community, it will have to offer meaningful benefits for those related needs that are being felt with some strength and immediacy. The answers to the who gets what, when and how question can be very relevant in this context.

Disparate groups within the community will have to be brought together. Local businesses who are not benefiting from tourism, but are suffering negative influences on their revenues by the noise, traffic, and visitor behaviors tourism has brought in may well support efforts to better publicly manage the industry. Some tourist oriented businesses that do not require large numbers of customers also may support sustainable tourism. Those operators probably focus on:

Customers who are wealthier

Not primarily tourists, except when the tourists are mostly wealthy and numerous

Otherwise, vacation home owners among the tourists

Nonparty-oriented tourists

Customers who are likely to be concerned about public order

Residents who are being sufficiently adversely impacted by the local tourism to want to do something about it are likely to be major supporters. They have passed the activation threshold and specific sustainable tourism remediation steps might give them needed direction, while the general sustainability framework can give them political arguing points. These motivating adverse impacts can be related to noise and traffic issues as well as disorderly public behaviors and the overcrowding of public places. Parents with preschool children and seniors, important segments of many smaller downtown populations, are prone to being adversely affected by tourists behaving in a disorderly manner. Major owners of residential properties are also likely to support sustainable tourism efforts.

How many office workers reacted to the scene in Times Square may be indicative of how they will react to other overly tourist utilized public spaces in our large CBDs. Many of these office workers did not like the overcrowding caused by the tourists because it interfered with their ability to get to and from work, and to get food and do chores at lunchtime. Nor were they delighted by the naughty costumes and behaviors of many Times Square habitués. That suggests they, too, may be strong supporters of sustainable tourism programs, especially when it comes to the issue of public disorderly behavior.

Under sustainable tourism many of the issues that need resolution will be political in nature, with important groups in the community often taking seriously conflicting positions. These disputes will probably be best dealt with if they are informed by local “technocrats,” like planning, public safety, and economic development departments, as well as by the interested parties, but the actual decision-making power should rest in the hands of local elected officials who can be held accountable by voters.

Recovering From the Pandemic Will Provide a Rare Opportunity to Create Sustainable Downtown and Main Street Tourism Industries

Crises are Janus-like events, creating opportunities as well as problems. Tourism across the nation has been in steep decline. Many managers and owners in the industry are being forced to think about their future, whether they wanted to or not. In communities where tourism has been an important economic engine, many political leaders are probably also thinking about the industry’s future in their towns. This creates a real opportunity to make tourism in their communities more sustainable.

However, the window for this opportunity will not stay open for long. The pent up demand to travel is strong – planes and hotels are already beginning to fill up, and reservations for the remainder of 2021 are getting harder and harder to get.

Now is the time to recognize if your town’s tourism industry needs to be made more sustainable, and then to take the steps needed to make that happen.

Over recent months I’ve been getting a sense that some suburban downtowns may well make relatively strong recoveries from our current virus induced economic crisis, and relatively speaking, stronger even than those of our superstar downtowns. This also prompted me to think that the current and potential strengths of some of these suburban downtowns are too often underestimated and overlooked. I’m venturing to presume that others may also find these thoughts of interest and they are presented below. Please, let me know what you think about them.

Suburban Downtowns Are Different and Often Surprisingly Strong

Last year Bill Ryan and I did some research on dataset covering all of the 259 downtowns in cities in the 25,000 to 75,000 population range in seven Midwestern states. Our findings will appear in an article in the Winter 2020 issue of the Economic Development Journal, titled Living and Working Downtown: Is It a Population Growth Engine for Small Cities? Included in the dataset were 167 suburbs that usually are parts of relatively large metropolitan areas in which much larger cities are the cores, and 92 independent cities that are themselves the cores of a smaller metropolitan or micropolitan area. We were struck by how different these two types of downtowns are in many important respects. For instance:

Though less multi-functional, the suburban downtowns averaged about the same number of residents 3,089, as the independent downtowns, 3,294.

However, suburban downtowns had a higher population growth rate, 5% to 0.23%, and a lot fewer had declining populations, 31% versus 46%

Moreover, the suburban downtowns scored much lower on our two measures of live-workers in their downtowns, between 3.1% and 8.7%, than the independents, 12% to 29%. Additionally, such low levels even were present in the suburbs that had attracted relatively large numbers of office workers to other parts of their city, such as Dublin, OH, with 42,200+ in 2017

One factor that helps explain the greater strength of the suburban downtowns is that they are very probably located in metro areas with significantly stronger economies than the smaller metros the independent cities are anchoring.

A trend that helps to explain the low live-work numbers in suburban downtowns is that most suburban residents are not drawn to the type of dense housing units their downtowns tend to offer. National surveys for many years now have continued to show that about half of the adult population prefers living in the suburbs and that the vast majority of people who live in the suburbs want to be there. (See the table above.) That strongly implies that they prefer the urban lifestyle that includes single family homes, lower population densities, a slower pace of life, significant car use, and an environment that is predominantly “green” rather than concrete and asphalt.

Moreover, when these suburbs do attract offices they tend to be located in office park-like developments, within about a 5-minute drive of, but not in their downtowns.

The Importance of CSD Functions in Suburban Downtowns

Our findings also had some strong potential implications for a far broader range of downtowns:

Suburban downtown residential populations are not driven by the presence of downtown jobs, as some experts believe is the case with our large and superstar downtowns.

Consequently, they must be driven by other factors. Since the downtown populations of the suburbs and independents are so close, these other factors are probably as strong or stronger than downtown employment is in non-suburban downtowns. These other factors certainly are not weak, and they also could be present in non-suburban downtowns, too.

A very probable strong factor are the suburban downtowns’ Central Social District (CSD) assets: its housing, restaurants, bars, parks, athletic fields, public spaces, cinemas and theaters, libraries, art galleries, maker spaces, farmers markets, community centers, houses of worship, childcare and senior centers. Indeed, it can be reasonably argued that the suburban downtowns that have been successful in terms of popularity, use and investment have done so largely because of the strength of their CSD functions.

Housing is a very important CSD function. Two advantages suburban downtown housing may have are the likely greater comparative affordability of its costs and the convenience of it locations. In struggling downtowns units may be affordable because they are in poor condition and can only command cheap rents. In more successful downtowns, it may be that apartment rents/costs are cheaper than renting/owning an apartment in the region’s core city, or living in a suburban single family house (e.g., empty nesters), and/or because the apartment is occupied by several people who share the rent payments (young adults).

Units close to mass transit will probably be convenient for those who commute by rail or bus to large employment centers elsewhere in the region. Indeed, in these suburban districts, the commuters who live in TOD residential developments may be the equivalents, in terms of economic impacts, of the live-workers found in and near the cores of our largest downtowns. However, according to one report, NJ Transit has found that only 12.5% to 25% of the residents in the TOD projects developed around its stations are NJT commuters.1

These downtown residents can bring in substantial purchasing power. For example, it was estimated that, around 2010, the roughly 1,500 new occupied residential units in downtown Morristown, NJ, would bring in about $72 million in potential retail spending power. 2

Undeniably, when the CSD assets of a suburban downtown are strong, the district is highly urban in character, and more analogous to a strong big city neighborhood commercial district, such as Williamsburg in Brooklyn, or Forest Hills in Queens, than to a sizeable rural town. We might characterize these districts as “urbanized suburban downtowns.”

Typically, suburban downtowns have a Greater Downtown area that includes the downtown and nearby areas from which people can conveniently get to and from the downtown core , some on foot, but most by car. Sorry, folks, but we are talking about the suburbs here. That may be changing in the near future as AV vans and greater use of e-scooters and bikes come more into play.

The non-district portion of the Greater Downtown area can have relatively significant population and workforce densities and be the source of a lot of the customer traffic of downtown merchants. These users also can strongly influence the image of the downtown.

Unfortunately, there is no study of urbanized suburban downtowns. Some districts that I would include in that category are in Wellesley, MA; Englewood, NJ; Morristown, NJ; Cranford, NJ; Westfield, NJ; and Cranford, NJ.

Some have had strong GAFO retail, though that has weakened substantially with the upheavals in the retail industry over the past decade and the Covid crisis. Some have a lot of office workers located nearby in their town who are important lunchtime customers. Some have PACs, theaters and/or cinemas. All are walkable and have lots of eateries, coffee shops, and drinking places. All are surrounded by residential populations with high percentages of creatives – some also have large numbers of creatives working within or very near the town.

This suggests that non-suburban downtowns can also flourish by strengthening their CSD assets.

Suburban Creatives

For many creatives, these urbanized suburban downtowns may be extremely attractive, especially if they either: 1) prefer the suburban lifestyle when it comes to single family housing and green spaces, yet still enjoy urban type entertainment venues such as good restaurants and cultural events, or 2) they are nesting and need affordable and relatively spacious residential units, while also appreciating many aspects of urban entertainment and leisure time activities. The fact that these suburbs often have excellent public school systems also makes them attractive to core city nesting creatives who are looking for a more affordable place to live. In NYC, for example, the private elementary school average cost per student is $13,000 per year and for private high schools the average is $25,267 per year. With taxes, parents will probably need double that amount of their income to cover those costs.

My prior research on 14 counties in Northern NJ that are suburbs of NYC or Philadelphia – see the above table — certainly suggests that in 2010 very substantial numbers of creatives lived, worked or even possibly live-worked in these communities. Interestingly, the median of the percentage of their workforces that were creatives was 31%, but the median of the residential adult population in the labor force who were creatives was 40.3%. See above table. In Somerset and Hunterdon Counties over 50% of the residents in the labor force were creatives. So these suburban counties of superstar cities/downtowns probably have been recruiting lots of creative residents for decades. The size and economic power of these suburban creatives often seems to be overlooked because so much attention is focused on the young creatives being attracted to hip urban neighborhoods of the superstar cities.

Some downtowns in these high creatives counties have tried to attract more creatives to spark economic growth, while what they probably needed to do was to better leverage the numerous creatives they already had! Far too little attention has been paid to these suburban creatives.

The downtowns in these counties did not have anywhere near the number of apartments or condo units needed to house all of these creatives, so it seems reasonable to deduce that most were living in the single family type homes the suburbs are famous for. It also seems reasonable to deduce that the vast majority of these creatives probably were living there because they liked the lifestyles these suburbs support. In turn, this seems to counter the blindered visions of where creatives want to live that only focus on hip urban neighborhoods. Furthermore, it also counters visions that just focus on the young creatives who may indeed have a significant tendency to live in the hip urban neighborhoods, by showing lots of probably older creatives, who have probably nested, prefer suburban or rural residential areas.

Some Downtowns Will Be Better Positioned to Recover Economically Than Others

There already is plenty of evidence that points to the imputation that suburban downtowns, especially those that are urbanized, will be much better positioned to have a successful economic recovery than others. There are also a number of steps their leaders can take that will further solidify their strong recovery positions.

Tourists. Most suburban downtowns, especially those that have been urbanized, are unlikely to be heavily dependent on tourist customer traffic/expenditures as are the downtowns in our large cities such NYC, Washington, D.C., San Francisco, etc., or in rural towns where tourism is the main economic engine. In those areas the collapse of their tourist markets have had large negative impacts.

Moreover, the resurgence of tourism will be hampered by other factors besides the pandemic’s impacts. International politics is one. For example, It probably will be very hard for our major downtowns to regain the strong flows of big spending Chinese tourists they once had. Even under an optimistic scenario, it very probably will take a few years for tourism to return to prior levels in these downtowns.

Office Workers. Merchants in our big city downtowns have also been clobbered by the disappearance of their office workers. In many of them only abut 20% to 30% are now showing up. Moreover the growing adoption of remote work probably means that the number of office workers employed in our largest downtowns probably will decrease by 16% to 22% after the crisis. 3 In contrast, in the suburbs – e.g., Morristown, NJ, Dublin OH, Garden City, NY – that have attracted large numbers of jobs, office worker presence has remained substantially higher through the crisis than in central cities, and they are also more likely to fully recover more quickly. The suburban office workers do not have to use public transportation to commute to work. Consequently, these suburban towns are unlikely to be hurt as much by remote working or to experience their office jobs being decanted to less populated, and less public transit dependent areas as may happen in our large cities. To the contrary, some suburbs may be substantial recipients of such workforce decanting and the growth in remote working. Their downtowns will benefit from this.

Foot Traffic. It should not be surprising then to find that while in many large downtowns foot traffic has fallen by roughly 60% – 70% since 2019, it has been substantially less in their suburbs. See chart nearby.4 Foot traffic is critical to the health of any downtown. The suburbs may not need to recover as much as the center cities on this key variable.

Downtown Small Merchants. Truth be told, small merchants have been a disappearing breed in big city downtowns well before Covid19 appeared. At best they have retreated from the major commercial corridors to sidestreets. A number of factors were involved such as: unaffordable rents; associated real estate bubbles and consequent landlord needs for high paying tenants; new landlords who knew nothing about managing retail properties, and redevelopment that forced closures and relocations. In contrast, small merchants remain the primary occupants of the storefronts in most suburban downtowns, though vacancy rates have continued to creep up for many years now, and non-retail uses continue to increase.

While there has not been any rigorous systematic study, a review of many reports on the internet suggests that merchants who are more dependent on residential markets and less on tourists and office workers were doing significantly better than those who were focused on tourists. Many of our largest downtowns have relatively few residential units within their boundaries, but a whole lot within a Greater Downtown area that includes nearby neighborhoods from which residents can easily and quickly get to the downtown core. That would suggest that merchants in suburban downtowns, especially those with substantial new market rate housing, will not be among those hardest hit. Of course, that does not mean that they are not being hurt or stressed, but it may indicate that it will be relatively easier for them to survive and recover.

Downtown Retail Chains.

Superstar Downtowns, In these districts retailers have long paid extremely high rents for premier retail locations. However, in recent years, real estate bubbles and high rents have resulted in high “availability rates, ” with 20% or more not being unusual. The above table details such a situation in Manhattan in Q2 of 2019. Most of those locations have been very dependent on tapping office worker and tourist shoppers and their ability to again earn meaningful profits probably awaits the return of those shoppers at some still unknown time in the future. The prior high availability rate suggests problems that the Covid19 crisis can only have exacerbated.

Many of these retailers are in the luxury market and BCG recently estimated strong declines in luxury retail sales for 2020 and 2021, with a recovery appearing in 2022, BCG also found that many more shoppers are now trading down than trading up.5 Moreover, online sales of luxury merchandise has been growing significantly.

Many observers expect a new equilibrium between retailer and landlord needs will be reached in the coming years. However, until then retail in these big downtowns may be somewhat unstable. While the landlords of the luxury retailers may continue to claim that all is well, 20% availability rates and the disappearance of key market segments are strong visible evidence that those assertions are not true.

Retail Chains Resurging Post Crisis in Suburban Downtowns. The claim has been made that the closure of many malls and chains will set free so much market share that retail chains and small independent retailers located in suburban downtowns will grow and prosper as the current crisis ebbs. There is probably some merit to this claim – but not much.

Most suburban downtowns have not attracted large numbers of GAFO retail chains, though they often do quite well with those selling necessities such as groceries, convenience goods, and medicines. That is not likely to change in the future because these districts lacked and will continue to lack the required locational assets. Few have the auto traffic that passed near the malls. If retail chains do return to the suburbs, standalone locations abutting high traffic roads on the periphery of these towns may very likely be preferred to those in their downtowns. However, some in wealthier market areas – e.g., Westfield and Englewood in NJ, Wellesley in MA — have in the past attracted lots of GAFO chains, and they often were like open air lifestyle mall downtowns. Even then, though, while the number of retail chains present in these districts was often impressive, according to information confidentially provided by one well known national brokerage firm, their profits per store usually ranked relatively low within their chains. They were thus among the most prone to be closed if their chain got into financial trouble. So unsurprisingly their strength and numbers were eroded by the Great Recession, new competitors appearing both online and from strengthened malls, the retail chains’ corporate weaknesses being magnified by the process of creative destruction occurring in the retail industry, and the negative economic impacts of Covid19. For example since 2009, one of these retail chain rich suburban downtowns has lost the following chains: Esprit, Coach, Chico’s, Ann Taylor, Lucky Brand, White House-Black Market, Janis & Jack, Papyrus, Aerosoles, Victoria’s Secret, Eileen Fisher, Coldwater Creek, Kiels, Omaha Steaks, and Game Stop.

For many years the trophy retailers downtown leaders wanted to attract were largely in the apparel sector, e.g., The Gap, Chico’s, Talbert’s, Ann Taylor, Victoria’s Secret. Today, that sector is in disarray – even some off-pricers, like Stein Mart, that had been seen as well positioned, have fallen.

The argument for the supposed market share being yielded by closing malls and retail chains being captured by retailers in suburban downtowns has a number of problems analytically:

The demand for some kinds of merchandise has been in long decline, e.g., for apparel. This has been influenced by the trend toward informal workplace attire that has been strongly reinforced by the current crisis, and the growth in remote working. It also has been impacted by consumers wanting to spend more for interesting and rewarding experiences than for things.

More than ever, retail chains are looking for low risk locations. These locations tend to be in areas where there are significant numbers of fairly affluent shoppers or very large numbers of easily accessible shoppers with more modest incomes. About 20% of our malls were doing well prior to the crisis, and they tend to capture these affluent shoppers. Walmart, Target, Costco, Best Buy, et al are prospering even during the crisis from their growing proficiency with omnichannel marketing strategies. They are attracting the mid-market shoppers. These malls and big boxes are formidable competitors and probably are sopping up lots of any market share the folded malls and retail chains yielded.

E-retail was growing impressively before the Covid19 economic crisis, but its growth has accelerated substantially during the crisis, and strong evidence suggests these high e-sales levels will not diminish all that much as the economy improves. E-commerce definitely has and will capture substantial portions of any market share that folding malls and chains might yield.

There seems to be fundamental weaknesses with the business model used by retail chains, especially when they are taken over by hedge funds and the like. Bean counters seldom are good merchants, much less great ones!

Internet born retailers may look for spaces in suburban downtowns, but their behavior to date indicates they will look for locations in higher income market areas with strong customer flows. For example, Warby Parker now is located in downtown Hoboken and downtown Westfield in NJ. They are unlikely to flood our suburban downtowns.

The failed malls and chains probably will yield a relatively small amount of market share that downtown retailers might capture. Small downtown merchants are much more likely to benefit from that yielded market share simply because they need much lower sales revenues to survive. That said, these small merchants still better have other market segments to tap.

There is little reason to believe that our recovery from this crisis will somehow coincide with the resurging strength of our specialty retail chains. Because of their high rents, landlords in our large downtowns will probability continue to seek retail chain tenants, or shift to other users who can pay those rents. Consequently, the large downtowns will continue to feel the impacts of the process of creative destruction that the retail industry still is in. On the other hand, relatively few suburban downtowns had many GAFO retail chains, and their numbers were substantially reduced even before the Covid19 crisis. Consequently, they neither benefit a lot from the presence of these retail chains, nor are they very vulnerable to the substantial vicissitudes that these chains may continue to face.

The Costs and Availability of Space. The ability of small merchants to recover and for startups to succeed will be significantly influenced by the availability and costs of their storefront spaces. While deflated rents and increased availability can be expected in both suburban and center city districts, the suburban rents long have been significantly lower and probably will remain so in a relative fashion well into the future. This fact, combined with the greater stability of their potential consumer market segments, probably will give the suburban merchants a greater chance of achieving a sound recovery, or a startup succeeding, than their center city peers might have.

Rent costs are particularly important for restaurant operations.

Remote Working.

The suburbs are also likely to benefit significantly from the shift to remote working:

Their numerous creative residents are likely to be in occupations prone to remote working.

Remote workers are likely to favor downtowns with strong CSD assets as they seek relief from the social isolation of their home offices, and they often also require business services and supplies.

Suburban communities are likely to have more relatively affordable housing, with more space per rental dollar than their regions’ center cities. This may attract many remote workers who are residents of the regions core cities. However, the affordability advantage might be blunted by rent deflation in the core city. For example, reports indicate that rents in Manhattan below 96th Street have already fallen by 20% to 30%.

Also recent research has shown that significant economic growth based on quality of life assets and the attraction of remote workers can lead to rising housing costs even in rural areas.

What will not be blunted, however, are the large numbers of people who prefer living in the suburbs, and they often include commensurately significant numbers of creatives, the group most prone to becoming remote workers.

It is fairly probable jobs will be decanted by a significant number of corporations from their prime big city locations to less expensive, auto accessible suburban satellite locations. Such office facilities will have cheaper rents than those in the core city downtowns, and provide corporate tenants places where their remote workers can come to get the social interactions they need to help their productivity, creativity and career advancement.

Recovering CSD Functions.

Many CSD venues have been hit very hard by the pandemic’s economic adversities. Almost all performance and exhibition venues have been closed or their public access severely limited. Many pamper niche operations closed permanently or shifted to operating online. Yet many of these operations, when allowed by local governments, have reopened on a limited basis, and the characteristics of some suggest that they will recover along with the local economy.

Two characteristics will determine those that will recover quicker and stronger and those that will not: if they are for profit operations and if they are large.

Small Arts Organizations. About 40% of the arts nonprofits are usually in the red financially, and mortally threatened by strong economic recessions and economic crises such as the present one. 6 Their business model is so dependent on contributions from numerous sources that their financial recoveries are seldom easy. So downtowns of all sizes are likely to have to wait quite a while for these smaller arts organizations to recover and contribute to their vitality.

Pamper Niches. In contrast, many of the pamper niche operations are for profits and relatively small – hair and nail salons, Pilates and yoga studios, dance schools, martial arts, studios, spas and gyms. They have relatively very low start up and operating costs, and little need to keep large inventories of goods on hand. While many were quick to close during an economic crisis, they are also relatively easy to restart or start anew as the economy improves. They are also the types of operations that often occupy large numbers of downtown storefronts, especially in the suburbs. Indeed, in many of our suburban downtowns there have long been complaints that these pamper niche operations were crowding out retail tenants because they could pay the higher rents landlords were looking for that small retailers found unaffordable.

Restaurants. Some of the most important CSD venues for all downtowns are their restaurants and bars. From early on in the crisis, there have been dire predictions of calamitous levels of restaurant failures – one foresaw the prospect of 85% of our eateries failing.7 These claims seemed to be supported by prior research showing that the average small restaurant only had enough cash on hand to cover their expenses for so few day, 16, that they were unlikely to stay open if they faced a major economic crisis – see table below. Months later, well into the current crisis, the Census Bureau’s Pulse surveys of small businesses have had consistently similar findings.8 One might have thought that by then their numbers would have declined as many went out of business. National survey data seems to indicate that about 20% of our restaurants may have closed do far.

The Center City district in Philadelphia recently published very interesting and well researched counter findings about restaurant closures.9 Well into the crisis, their survey found that only about 5% of their 1,078 restaurants had closed permanently, with another 19% closed temporarily. Just 19% were deemed fully opened and have indoor dining. Perhaps most interesting are the 600 restaurants (about 55%) that are classified as partially opened because they have outdoor dining, or only do take outs and deliveries.

My observations in the solidly middle income neighborhoods close to my home here in Queens, NY, also found a surprisingly low number of permanent restaurant closures. My communications with some suburban downtown managers yielded similar observations. The only reports of numerous closures I’ve found were about the eateries in the Midtown Manhattan CBD that are so dependent on tourist and office worker customers. The City’s Comptroller just issued a report that “found that more than 2,800 small businesses had permanently closed between March 1 and July 10, including at least 1,289 restaurants.” That would mean that about 5% of NYC’s restaurants closed, on par with the Center City findings.10

The fascinating question is: How are so many restaurants surviving so long when they never seem to have enough cash on hand to do so? CARES or other government program dollars? Owners not taking any salary? Dipping into their 401ks? Tapping extended family resources? Landlord forbearance? Public donations via gift cards, crowdfunding, etc.? The Center City research findings suggest a possible viable explanation: many are in some stage of operational hibernation – e.g., the 19% that are temporally closed and the 55% who are partially opened. Their reduced operational metabolism rates translate into a reduced need for cash. In turn, that means that the cash they have on hand can cover more days of operation. It also may mean that financial tools that are well within the restaurant owners control – such as dipping into 401ks, using credit cards, tapping family resources, etc. – can get many through the survival phase of this crisis if they hibernate. That also would mean that they are making substantial personal and family sacrifices in the hope that they again will earn meaningful annual incomes as they emerge from hibernation during the economy recovery.

If recovery means that these restauranteurs have to come out of hibernation and compete to again win adequate annual incomes, then it may prove to be a time period as, or even more, arduous than was the survival phase of the crisis. More restaurants may close because they will need to earn a lot more money to thrive than they did to survive, while they may have depleted the financial resources that helped them to survive thus far. Local market conditions will probably play a very important role in determining those eateries that will survive and those that will fail.

Households in the top income quintile (above $109,743 in 2017) accounted for about 38% of all the consumer spending for food away from home; those in the top two quintiles (above $66,898 in 2017) accounted about 61% of those expenditures. See table above. Moreover, so far into the crisis, employment in households with incomes above $60,000 has been far more secure than for those with lower incomes. Downtown restaurants able to easily tap affluent residential customers are more likely to survive the recovery than those that are not. The urbanized suburban downtowns tend to be in rather affluent market areas: in 2016, I estimated the annual household income at $188,000 for downtown Wellesley, MA; $131,000 for downtown Englewood, NJ; $152,000 for downtown Westfield, NJ, and $165,000 for downtown, Morristown, NJ. That will help their restaurants recover relatively quickly and substantially.

Let’s compare the prospects during the recovery phase of this crisis for restaurants in our superstar downtowns with those in our urbanized suburban downtowns:

Markets: The superstars must wait for the return of two very large market segments, office workers and tourists. Their residential markets may not be all that strong. Financially, that means many may have to wait quite a bit of time for their revenues and profits to return to the levels their owners were sacrificing to stay in business for. Their potential residential customers live mostly in nearby neighborhoods that are likely to have their own restaurants that are much closer to them. In contrast, the suburban downtown eateries rely mainly on the residential market segment that has never gone away and that savvy operators have been serving with takeouts, deliveries, and curbside deliveries during the crisis. These suburban eateries may also have office workers who are still present in the town in significant numbers, and others returning at a rapid rate as the virus’s impacts subside because of their reliance on autos to commute. New remote workers and newly decanted office installations may add significantly to their numbers. The suburbs’ consumer markets will start strong and may get even stronger. The superstars’ markets will start off very uncertain and require an unclear length of time to reach an iffy level of recovery. For example, though their office workerforces eventually may return, they’re very likely to be, at best, about 16% smaller in number.

Most arts tourists (tourists who attend arts events) visiting our large cities are not big spenders. A study of 21 study regions with populations over one million by Americans for the Arts that included the cities of San Jose, Dallas, San Diego, San Antonio, Phoenix, Philadelphia, Miami—Dade and Chicago found that, in 2016, the average arts tourist spent about $51.41 a day. See the table above. About 31% of that went for meals and drinks, averaging $16.05. Another $6.57 went for refreshments and snacks. While there certainly are significant numbers of wealthy arts tourists and they are likely to be among those who resume visiting our superstar downtowns fairly early, they will tend to go to the higher priced eateries. The less expensive eateries in these downtowns are less likely to see their tourist patrons return as quickly or as robustly. Their recovery is likely to be weaker and slower