Non Resident Downtown Employees. Three plus years after Covid19 was declared a national emergency, it seems that most of our downtowns are now pretty far into recovering from its impacts, though their recoveries are not yet complete. Even so, fears of a Doom Loop emerged grounded mainly on the negative impacts of remote work on office demand, that in turn is based on some distortedly presented data from Kastle Systems on office building worker occupancy rates. Kastle reports on metro regions, not cities though they speak of cities, and the vast majority of their buildings are in the suburbs, not downtowns. Also, when they do have some presence in a downtown, they tend to be in the second tier buildings most likely to have been made outmoded by remote work, not the most attractive and successful ones. In Manhattan for example, Kastle is not in the higher quality buildings owned by the city’s 10 largest landlords that attract the most prestigious tenants and have the highest rents.[1] Flaming the Doom Loop fears was an academic study that showed how such a reduction in office occupancy in NYC and nationally would severely reduce property values by about 44%, with commensurate resulting reductions in municipal property tax revenues.[2] To date, such drastic reductions have not appeared to gain much traction in NYC or nationally.

The most reliable data on remote work is from WFH Research. It shows that about 41% of the workers it sampled work totally remote (12%) or in a hybrid mode (29%). Moreover, about 33% of the paid full days were worked from home in our largest cities. So yes, remote work has reduced the number of hours office workers are in our downtowns, but most are still working there. And the 33% is far less than the 60%+ hours worked at home early in the crisis. So office workers have slowly been contributing to the recoveries of their downtowns by working more often in their downtown offices, if not at precrisis levels.[3]

That said, the data strongly support the hypothesis that a significant amount of remote work is here to stay, and corporate execs and downtown leaders committed to achieving a 100% Return To Office (RTO) rate may be digging a ditch for themselves by fiercely fighting remote work. What they also probably overlook is that precrisis the office buildings in these large downtowns never had a 100% worker occupancy rate. An 100% rate would mean that workers were not sick, on vacation, doing their jobs by meeting externally with clients and suppliers, or working from home.

Consequently, it is really hard to understand those who continue to want a 100% RTO rate and the extinction of remote work, since evidence strongly indicates that quest is impossible to achieve, and it probably never even existed before Covid19. Certainly, one can question whether a recovery strategy primarily aimed at achieving precrisis office occupancy rates would be productive.

Furthermore, we don’t know clearly yet how that 33% reduction in paid days worked will translate into office demand. One might reasonably suspect that it makes a lot more buildings outmoded. Yet, there is a real possibility that the effects of remote work might be mitigated to a significant degree by higher SF/worker in offices reconfigured to be more attractive to workers and heighten a firm’s RTO rate. A current primary strategic challenge for our large downtowns is how to make up for the spending and pedestrian trips of the 41% of office workers who are now working at home to a significant degree. That is what downtown leaders should now be focusing. on, not raising RTO rates.

Downtown Housing. More housing is certainly one way of doing that, but it will take a lot of time, gobs of money, new regulations, and a lot of tough politicking to achieve. It will certainly not be easy.[4] That said, it definitely still should be done, but we now need another strategic thrust capable of producing meaningful shorter term benefits.

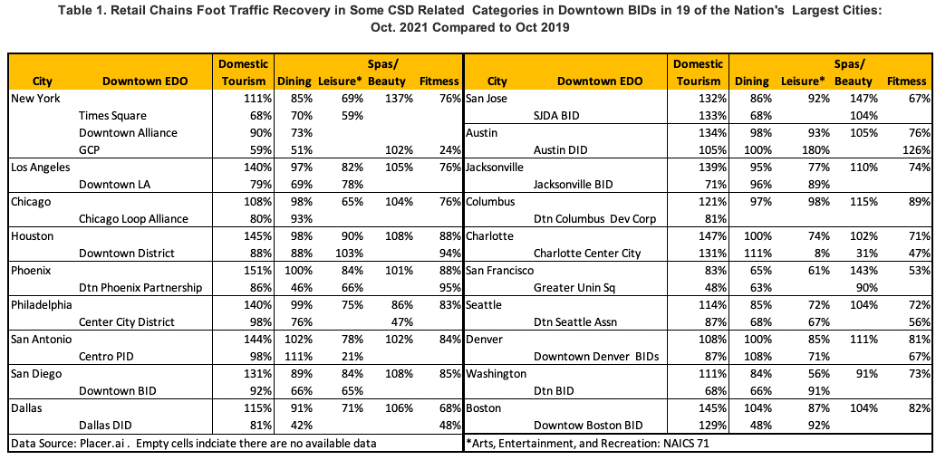

Downtown Visitors. To achieve more immediate results, another, and more practical, strategic thrust should be to increase downtown visitation by those who neither live nor work there. Data released by Philadelphia’s Center City District –see Figure 1 above –show that such visitors account for most downtown visitation and by a large margin.[5] Based on the data in Table 1 that shows domestic tourism was returning very strongly at the municipal level in 19 of our largest cities and in several of their downtowns—e.g., Austin, Boston, Charlotte, San Jose, and Philadelphia – as early as October 2021, my very strong suspicion is that researchers will soon report that this pattern characterizes many other large downtowns.

Foreign and business tourism are also recovering, but at lower rates that may take some time to regain precrisis levels, if they ever do. Business travel budgets, for example, are rebounding, though reflecting in part higher travel prices. Moreover, about 17% “of corporate travel will be replaced with virtual meetings, …suggesting a degree of permanence in the shift with companies recognizing the benefits of virtual meetings ranging from cost savings to lower carbon footprints.”[6] Still, foreign and business tourists had almost completely disappeared from our large downtowns early in the crisis, so their returns, even if at a level lower than might be desired, have been meaningfully contributing to downtown recoveries.

Strong Destinations Are Needed to Win More Visitors. My research and field visits over the past few years has led me to believe that many of our largest downtowns need to up their game when it comes to downtown visiors:

They have been living off of their laurels and too many of the attractions downtown leaders have seen as strong and unique have in fact lost their luster and a significant amount of their magnetism.

These old attractions/destinations now need a hard-headed assessment, and then where required they should be improved or replaced. People come downtown based on the strength and convenience of its attractions.

Improving the programming of public spaces may be one element of such a thrust. Improving the tenants of the small shops on side streets might be another. Right now many rely primarily on retail windows to make sidewalks interesting. Can other uses capable of doing that be brought in?

In many of these large downtowns these attractions’ ability to bring in visits by people living and working within between .25 mi and 1 mile of the core has significantly atrophied over the past 10 years or so. THESE RESIDENTS ARE NOW BEING UNDERSERVED, YET ARE WITHIN REASONABLE WALKING AND BIKING DISTANCES. They should be given priority attention.

[5] In Placer’s calculations: “Visitor” = shopper, tourist, convention attendee, concert attendees, someone visiting a doctor, etc. Resident = Their phone sleeps in the geography most nights per week. Non-Resident Worker = Their phone sleeps in a different geography at night, but routinely comes to the same location in the defined area 3-5 days per week. I want to thank Paul Levy for generously sharing these data with me.

By William F. Ryan, University of Wisconsin – Madison/Extension and N. David Milder, DANTH, Inc.

Introduction

Within the downtown revitalization community a broad consensus has formed around the maxim that the greater the number of people who live in our downtowns, the more likely they are to prosper. These residents help to spark the “activation” of the district, providing the visible evidence of people engaging in a variety of activities, and nurturing the perceived sense of vitality among visitors that makes the area a magnetic place to be. A number of factors can impact this downtown population growth. The real estate market certainly is one. Job growth, especially of creative class employees, is another. One that has gained notice, of late, is the number of people who live and work in their districts, and the live-work environments that emerge to both support them and reflect their attitudes and behaviors.

Most of the attention paid to the live-work engine has focused on our largest cities. After a brief look at those downtowns, this article will look in greater depth at the numbers, behaviors and impacts of live-workers on suburban and independent cities with populations between 25,000 and 75,000 .1 Suburban cities are located in a metro area in which there is a large center city. They usually serve more as bedroom and leisure communities than employment centers. Independent cities are more geographically isolated and may be the cores of a small metropolitan/micropolitan area. They serve as employment and commercial centers as well as bedroom and leisure communities. They are often also government centers (e.g., county seats). They are more multi-functional than the suburban downtowns.

Live-work Environments as a Growth Engine in Our Largest Employment Nodes.

Job growth alone often has had mixed impacts on a downtown’s vitality and attractiveness in our larger cities. In the 1980s, for example, office development – with its large numbers of white collar workers — was seen as THE downtown redevelopment strategy, but it produced a large number of disappointing projects in dull and perceived unsafe downtowns. Many of them had to be “redone.”2 In office dominated districts, there were too many fortress-like office towers, and they lacked the multifunctionality and pedestrian activity that are critical for downtown vibrancy. Though somewhat active weekdays from about 11:00 a.m. to about 2:00 p.m., the downtowns were deader than doornails at other times. There were too few people around once the offices closed.

Since the early 2000s, and especially after a major paper by Eugenie Birch in 2005, observers noted that our larger downtowns in the 1990s had been attracting significantly more residents.3 In the years since, housing development has become increasingly seen as the secret revitalization sauce for a large number of downtowns, including those in numerous suburbs, and almost all of our largest cities. These new residents help activate their downtowns after 5:00 pm on weekdays and over the entire weekend.

However, not all downtowns experience household growth. For example, Birch found that about 27% of the downtowns she studied had declining numbers of households.

Downtown housing growth and district activation is thought to be strongest when downtowns have attracted large numbers of “live-workers. They are there after 5:00 p.m. and on weekends. They don’t spend much time in vehicles commuting, but often will walk to and from work, or make short trips on public transit. For example, in several zip codes in Manhattan over 50% of the residents who are in the labor force walk to work. The live-workers very often are also creatives with high salaries.

In a seminal monograph published in 2017, Paul Levy and Lauren Gilchrist researched the percentage of live-workers (those who both live and work in a district) in 231 major employment centers located in the nation’s 150 largest cities and within a one-mile radius that surrounds each of these centers. 4 Their work is important because it:

Demonstrates how downtowns are intractably inter-related with their immediately surrounding neighborhoods.

Showed that a significant number of the downtowns in the nation had very significant levels of live-workers of 40.7% to 55.9%, especially those in superstar cities. (See the above table). The authors did not overtly make that claim, but, several of the high performing downtowns they listed are what Aaron Renn has termed as superstar cities: “These “superstar cities”—New York, Los Angeles, the San Francisco Bay Area, Boston, Washington, and Seattle—are among America’s largest, most productive urban regions. They have well-above-average per-capita GDP and incomes and serve as the home bases of high-value sectors like finance (New York) and high tech (San Francisco)”. 5

However, the vast majority of our largest employment nodes had considerably lower levels of live-workers: 60% had fewer than 20% of their workforce being live-workers, with 42% in the 10%-19% range. 6

Live-workers in Independent and Suburban Cities.

The authors utilized a data set compiled by William Ryan, of the University of Wisconsin -Madison/Extension , and Prof. Michael Burayidi, of Ball State University, that covers 259 downtowns in cities with populations between 25,000 and 75,000 in Illinois, Indiana, Iowa, Michigan, Minnesota, Ohio and Wisconsin. The dataset contained valuable information about the sizes of these downtown populations and their growth or decline. Using the Census Bureau’s On-the-Map online database, two variables were added to the original dataset: the number of people who both lived and worked in the city (N Live-workers in City) and the percentage of people participating the nation’s workforce and living in the city who also worked there (% Live-workers in City). The limitation of these added data is that they are characteristics of the whole city and not just the downtown and its immediately surrounding areas. The reasoning for using these data is that the two live-work variables can be seen as indicators of a proclivity to live-work within a city and the analysis can be framed by looking at the impact of that proclivity on the size of these downtown populations and rates of population growth/decline.

A closer look at downtown live-work situations is also presented below. However, because of resource constraints, it is confined to 10 cities in this population range. Five are independents and five are suburban. Several of these downtowns are not in the Ryan-Burayidi dataset.

Downtown Population Growth and Decline. These downtowns do not appear to be having the impressive level of population growth that is to be found in our larger cities, and this is especially the case for the independent cities that are not part of a large metro area.

The suburbs averaged downtown populations that were about as large, 3,089, as the independents, 3,294, but had a slightly larger maximum and a lower minimum. The suburban downtowns captured only a slightly lower proportion of their city’s population, with a median of 7.6%, than the independents did, with a median of 9.2%. Their highest proportions were close, too, 28.4% among the suburbs and 27.3% among the independents.

However, the suburban downtowns had an average growth rate between 2010 and 2018 estimated at 5% compared to just 0.53% for the independents. Both growth rates were far below the two digit growth rates many of our larger downtowns have been experiencing. Unexpected is the large percentage of these downtowns with negative growth rates, 36%. One might think that we were back in the 1960s or 1970s. In this regard again, the comparative strength of the suburbs stood out: while 31% of the suburban cities were dealing with declines in their downtown’s population, 46% of the independents experienced such decline. The suburbs also showed much more variation in their growth, with a low of -57.2% and a high of 140.2% compared to the -11.6% and 17.9% for the independent cities.

Many of these downtowns could benefit from a strategy that can increase their downtown populations.

An important factor in the different downtown population growth rates of the suburban and independent cities is their current economic growth potentials. Recent studies by Brookings and AEI have noted that economic development these days is stronger in communities that are attached, in a metro area, to a large city that has a population above 250,000.7 Many of the suburban cities in the Ryan- Burayidi dataset are attached to such cities (e.g., Chicago, Minneapolis, Columbus). In contrast, the independents, all under 75,000, probably are not, and instead are themselves the core cities of smaller and weaker metro areas.

Levels of Citywide Live-Work. Again, because of their very natures, these two types of cities display quite different levels of live-workers at the city level. In the more geographically and economically isolated independent cities, half of them have over 33% of their residents who also work in the city, with 10% having between about 54.7% to 67.7% of their residents being live-workers. Those numbers, though at the city level, compare favorably with the percentages of liveworkers in and near our big city downtowns identified by Levy & Gilchrist. In contrast, the suburbs, being integrated into an economic region with lots of jobs, have many fewer live-workers at the city level. Half of the suburban cities have less than about 9.9% of their residents also working in their cities, with the highest percentage being 36%, about half that of the independent cities.

A Pearson Correlation analysis showed that both live-work variables have very weak relationships with downtown population size in both independent and suburban communities, with no r exceeding .166 or being statistically significant. These findings support the conclusion that the proclivity for live-working in both types of cities probably has little impact on the downtown’s population size. People who live close to where they work are not clustered in and near their downtowns in these 259 cities.

However, there was a positive r of .249 significant at the .05 level between the number of live-workers in the independent cities and their downtowns’ rates of growth/decline. This does suggest that the proclivity to live-working can have some positive association with downtown population growth in these communities when they are growing. That may point to the additional availability of new downtown housing units that facilitate live-working.

A Case Study of a Creatives’ Suburb. Looking at the nature of the live-work environment in one of the suburban cities in our dataset, Dublin, OH, provides an interesting case study. Dublin is the nation’s 13th strongest creative class city, according to Richard Florida. 8 For a suburb (of Columbus) , it also has a large number of people who hold jobs in the city, about 42,249 in 2017. (See the above table). Given the propensity for creatives to prefer hip urban areas, one might expect a high number of live-workers in this downtown. However, the number of live-workers within a half-mile of the downtown’s center point in 2017 is a miniscule five. In 2017 live-workers represented just 0.18% of the downtown’s workforce and 1.2% of its residents who are in the labor force. They also represented just 0.48% of the downtown’s 1,024 residents (includes those not in the labor force). Those five live-workers accounted for 0.2% of the 3,184 live-workers in the whole city. Live-workers seem, if anything, to be avoiding the downtown.

The number of people who are in the labor force and live in the 0.5 mile had dropped slightly, by 19, from 2007. Most notably, the absolute numbers of live-workers and their percentages of the relevant area’s workforce and residents increased with their distance from the downtown. Moreover, the number of live-workers in the city increased by 408, while the increase within the 1-mile ring was just 44, or about 9% of the city’s total increase. This is consistent with the hypothesis that the local residents and workers have little interest in living in urbanized environments, or at least the type offered in downtown Dublin. The downtown might not be seen as hip. It is very small. This should not be surprising in a town that is such a strong exemplar of a successful suburban city. Here is how Google describes the city:

“Dublin Ohio is a long standing community and is probably best known for being the home of Jack Nicklaus’ Country Club at Muirfield Village”.

“Dublin is in Franklin County and is one of the best places to live in Ohio. Living in Dublin offers residents a sparse suburban feel and most residents own their homes (italics added). In Dublin there are a lot of bars, restaurants, coffee shops, and parks. … The public schools in Dublin are highly rated.” 9

In 2014, a survey by Trulia found that 53% of the 2,008 respondents lived in a suburb and that about 93% of them preferred living in suburban locations. 10 That suggests a high probability that a strong majority of the residents in towns like Dublin might not be looking to live in a dense downtown location in a multi-unit structure. The situation in Dublin signals that many creatives may be among them.

Dublin recently undertook a massive new project, the Bridge District to strengthen the downtown. It will be interesting in a few years to see how that changes how many people live in its downtown and how many are live-workers. 11

An In-Depth Look At Working Populations, Jobs and Live-Workers in 10 Selected Downtowns.

The authors selected 10 downtowns they have visited and researched with populations in the 25,000 to 75,000 range (with the exception of Morristown, NJ) to look at their live-work rates, if these rates grew or declined between 2007 -2017, the size of their working populations (residents in the labor force), their number of jobs and how they also may have changed between 2007-2017. The data were downloaded from the Census Bureau’s On-the-Map online database using 0.5mile and 1.0 mile radii centered on the key intersection in each district. The assembled data are displayed in the two tables presented below. The analysis of such a small sample has obvious statistical limitations. In the natural sciences, e.g., astronomy, however, analogs are often treated as outliers that bring an existing theory or paradigm into question or suggests a need for their amendment. Our findings are presented as being directional, not conclusive, and sometimes as signaling that attention should be paid to them because they do not fit with the accepted professional wisdom.

For the downtowns in the cities in the 25,000 to 75,000 population range, the 0.5 mile ring will cover most or all of their district. It also represents an area that the average pedestrian can cover in about a 10-minute walk from the downtown’s center. It is also often used to define the boundaries of transit-oriented development districts. The 1 mile ring defines and area that is about 4.13 times larger than that of the .5 mile ring, and the average pedestrian would have to walk for about 20 minutes to go from the downtown’s center to the ring’s boundary. Such a walk is still doable for many, but its difficulty is sufficient to probably make others use some form of transportation or simply not make the trip. The .5 mile to 1 mile donut probably represents the nearby neighborhoods that are so crucial to the success of our downtowns.

Residents in the Labor Force. As can be seen in the above table, the number of people who live in the 1-mile ring and are in the labor force (labor force pop), for the most part, is far from negligible. (Note, they do not necessarily work in or near the downtown). The most are in two suburbs, Cranford, 8,817, and Morristown, 8,728, both in NJ. However, the average for the 5 independent downtowns’ 1 mile rings, 6,566, is about 10% higher than that of the five suburban cities, 5,977.

A far larger disparity appears when we look at the data for .5 mile rings: the average number of ring residents who are in the labor force is 1,776 for the five suburban city downtowns, but 307% larger at 5,455 for the independent city downtowns. This probably reflects key differences in their basic characteristics: the independents probably are larger and have traditional, more densely developed downtowns, with more housing units and more jobs, while the suburban downtowns are less densely developed and less multi-functional. However, within the suburban group, Cranford, Morristown and Downers Grove all have many more of these residents than the other two downtowns. Notably all three had completed a number of downtown housing projects in the 2007 to 2017 timeframe. Also, Morristown is both a suburb in the NY-NJ-CT Metropolitan Region, and a county seat and regional commercial center. Notably, it and Garden City have more people working in the city than residents. Starting out as bedroom communities has not stopped them from also becoming office employment centers.

The table also provides ring ratio values that are created by dividing a variable’s value for the 1 mile ring by its value for the .5 mile ring. This sheds light on where the weight of the geographic distribution is between the two rings. Here we are looking at the ring ratio for residents who are in the labor force. A value of 4.1 would indicate an evenly balanced distribution. Values below 4.1 mean the distribution is weighted to the .5 mile ring, and the lower the ratio’s value, the more heavily the distribution is weighted. Conversely, values above 4.1 indicate the degree the distribution is weighted to the 1 mile ring. While the ring ratio for the suburban cities, 3.4, and the independents, 1.2, indicate the weight of the distribution is toward the downtown, it is much stronger for the independent downtowns.

Live-Workers. When it comes to live-workers, the differences between the independent and suburban cities are even more striking. In the .5 mile ring the suburbs range between an unimpressive 5 and 216 live-workers, with an average of 80. On average, live-workers account for just 4.5% of the residents in that ring who are in the labor force. If we look at the suburbs’ 1 mile rings, the numbers rise, but they still are relatively small. Their live-workers range between 169 and 1,146,, with an average of 521. The live- workers in that ring, on average, represent just 8.7% of its residents who are in the labor force. These findings are consistent with the conclusion that the vast majority of the people who live in and near suburban downtowns do not do so because their jobs are also there, though some may be employed elsewhere in their cities. Other factors are leading these residents to select residences in and near their suburban downtowns. Such factors might include the convenience, transportation assets (e.g., commuter rail), and the attractive central social district functions these downtowns offer.

Live-workers have a stronger presence in the independent cities, especially in the 1-mile ring around their downtown’s central location. The range from 181 to 328 in the .5 mile ring, with and average of 231 and from 959 to 1,459 in the 1 mile ring, with and average of 1,212. On average the live workers are 7.7% of the residents in the .5 mile ring who are in the labor force , but 19.9% of those residents in the 1 mile ring. Moreover, Laramie and Rutland have much more impressive levels of live workers, 39.5% and 29.3% respectively. These are levels comparable to large numbers of our largest downtowns. One explanatory hypothesis is that live-working is likely to flourish in the core cities of a metro area, be it large or small, but not in suburban cities.

The ring ratio of suburban cities for the live-workers is 6.5, and for the independents it’s 5,2, indicating their distributions are weighted significantly toward the 1 mile ring, in the .5 mile to 1 mile donuts where residents are likely to find walking to the town’s center not really easy and liable to need/use some transport to get there. This also supports the conclusion that while live-workers may be great for downtown activation and success, downtowns often may not be where people who want to live-work will decide to reside. Being near, but not in the downtown may allow them to enjoy both the assets of the downtown and a suburban home and lifestyle. This may be a reflection of the local cultural where single family residences and traveling by car still are highly valued. While this may be more apparent in suburban cities, these cultural preferences can also be found the independent cities that are so often cities in the midst of a rural area.

Influence of Jobs. Levy and Gilchrist argue that job growth and density are major reasons why live-work levels get very high in our most successful downtowns.

Looking at suburban cities in the bottom half of the above table, one might note that three of them have relatively large numbers of jobs in their 1 mile rings: Garden City 31,309, Morristown 23,431, and Dublin 16,529. They are in the large NY-NJ and Columbus metro areas. Indeed, the five suburban 1-mile rings average 16,890 jobs In contrast, the average job count in the 1-mile rings of the independent cities is just 6,566, with the highest being Rutland’s 7,659.

However, when we look at the percentage of jobs being held by live-workers in both the .5 and 1 mile rings, the averages for the suburban cities are just 1.5% and 3.1% respectively. Despite their high job numbers, the percentages of Garden City, Morristown and Dublin in the 1 mile ring are just 1.5%, 4.9% and 1.0% respectively. The connection between jobs and the emergence of a large number of live-workers seems to be barely existent in these suburban communities, even in those that are prosperous and have lots of jobs.

Live-workers have a more significant presence in the independent cities, especially in their 1-mile rings. The average percentage of jobs held by live-workers in the .5 mile rings is 12.2% and 19.1% in the one mile rings.

However, many of these cities have been struggling. As noted above, 46% of the 91 midwestern independent cities in the Ryan-Burayidi database had declining downtown populations. Auburn, Laramie and Rutland had job losses in their .5 mile ring of -25.6%, -17.8% and -17.8% respectively between 2007 and 2017 and declines in the number of live-workers of -25.6%, -24.9% and -24.2% respectively (see table below). Still, in all five independent cities there is total agreement in all 10 rings between the directions of job growth/decline and live-work growth/decline. That certainly signals a meaningful association between the two.

The opposite is the case with the suburban cities. In seven of their 10 rings there is disagreement in the directions of job growth/ decline and live-working.

Also worthy of note is that between 2007 and 1017 the number of live-workers declined in six of the independent city ring areas and in eight of the suburban ring areas. While live-work may have been growing in our larger cities, these 10 cities suggest that it may have been struggling in our medium sized cities.

The ring ratios for the suburban cities, 3.2, and the independents, 2.7, both indicate the geographic weighting of jobs is toward the downtown. This is again the opposite direction of the live-worker ring ratios. Jobs may be going to the downtown core, but live workers are going to the close-in neighborhoods surrounding the downtown or at its periphery.

Conclusions and Implications

Many of These Downtowns Are Struggling. This is strongly evidenced by the analysis of the 259 cities in the Midwest with populations between 25,000 to 75,000. Many of their downtown populations are declining, not growing. The problem is 48% greater in the independent cities than in the suburban cities that are often attached to fairly large and more prosperous metro areas. That Laramie and Rutland are also having downtown problems suggests that such weakness is not confined to the Midwest, but probably national in scope.

The success of our superstar cities and downtowns should not cloud our awareness of the challenges many of our other downtowns are still facing.

That Said, Their Downtown Populations Are Not Insignificant. The average downtown populations of the 91 independent cities, 3,294, and the 168 suburban cities, 3,089, are similar. Downtown populations of that size can have over $150 million in total annual consumer spending. If they just make one trip daily outside their homes that totals over 6,000 potential in-out pedestrian trips. Those are not negligible numbers.

Live-Working in These Cities Is Struggling, Too. While live-work may have been growing in our larger cities, in the 10 cities given a close look in this study, the numbers of live-workers declined between 2007 and 2017 in all of them. In the suburban downtowns live-work was not significant to begin with. That suggests live-work may have limited potential in many suburban downtowns and that it is struggling in a large number of our medium-sized independent cities nationally.

The Job Growth/Decline – Live-Work Growth/Decline Connection Does Not Work in Suburban Downtowns. Even when they have tens of thousands of jobs, the suburban .5 and 1 mile rings have very low percentages of live-workers. Conversely, the independent cities, that are often the core cities of small metro areas and have denser and more multi-functional downtowns than the suburban cities, can have significant levels of live-workers. In them, the connection between jobs and live-workers seems to be meaningful. However, the data on these five independents indicate that this can be a double-edged sword. When jobs grow, so can the live-workers, but, when jobs decline, so will the number of live-workers, and many of these downtowns are in stressed regional economies. One explanatory hypothesis is that live-working is likely to flourish in the core cities of a metro area, be it large or small, but not in suburban cities.

Is Job Growth Really the Primary Engine of Downtown Population Growth? The average downtown populations of the 91 independent cities and the 168 suburban cities are similar, but they differ in what attracts these residents. While proximity to jobs might draw a significant number of residents to locate in independent city downtowns, that is not the case with the suburban downtowns. Indeed, even most of the residents in the independent downtowns probably are not drawn there by the proximity to their jobs. If that holds nationally, then the argument for jobs being a primary engine of downtown population growth needs to be amended. Moreover, the reverse commuters in our superstar cities, such as those riding Google buses from their San Francisco homes to their Mountainview jobs, suggest national applicability.

The question then becomes, what other factors can be attracting downtown residents? Since our data did not cover this question, we can only hypothesize based on the accepted conventional wisdom in the downtown revitalization field the following:

The downtown’s multi-functionality, that there are so many diverse needs and wants that can be met in a downtown.

The attraction of the downtown’s central social district assets: its housing, restaurants, bars, public spaces, cultural and entertainment venues, senior and childcare centers, places of worship, pamper niche venues, etc.

The convenience of being able to walk to all of these venues and engage in all of the activities in a compact and visually attractive and humanly scaled area.

In the suburbs, the housing units proximity to a commuter rail or an express bus station.

If this hold water, then these downtowns should pursue revitalization strategies that reflect those points.

The Signals of Important Cultural Preferences. It’s important to keep in mind that the vast majority of the cities analyzed in this study are either suburban or medium-sized cities in rural areas. Very high proportions of the people who live in these areas prefer living in such communities. Their cultural preferences are for single family homes, high car use, and a selective tolerance of dense clusters of people. Living in multi-unit buildings situated in or near a walkable commercial district may only be valued by a limited number of niche market segments, such as empty nesters, commuter rail users, and young adults who need to share residency costs.

Looking at the 10 cities spotlighted in this study: while the weight of the geographic distributions of the labor force population and jobs tilt toward the .5 mile ring, it tilts strongly to the donut area between the two ring boundaries for the live-workers. This suggests that there may be some important differences between the live- workers residing in the donut and those people who live in the core downtown area. One might conjecture that since it is likely that the housing available in the donut will not be as dense as it is in the downtown core, and also more likely to be single-family dwellings, that this signals an important lifestyle preference. This, in turn, may correlate with higher income households who can afford to buy houses going to the donut.

Moreover, as we noted about Dublin, OH, even though the town has a ton load of creatives working there, where its residents have chosen to live suggests a high probability that a strong majority of them are not looking to live in a dense downtown location in a multi-unit structure.

Would An Infusion of Creatives Alter These Cultural Preferences and Increase Live-Working? Creatives are often seen as the strategic solution to many downtown challenges. Would and infusion of them counter a culture’s existing preference for a dispersed lifestyle? Research by David A. McGranahan and Timothy R. Wojan found that in metropolitan counties about 30.9% of the workforce were in creative class occupations, while in rural counties it was just 19.4%. 12 One might reasonably deduce that the cities analyzed in this study have creatives that probably account for between 20% to 30% of their workforces. Creatives are famous for living where they will find the lifestyles they prefer, so the fact that they live in these suburban and rural cities can be taken as a fairly strong sign that they like living in these kinds of communities. That, in turn, suggest that they may have adopted many of the cultural values of their larger community. Moreover, whatever impact they might have already is reflected in the current situation in these cities and their downtowns. Also, given their education, income and employment, creatives also can be expected to have had an above average level of influence in the community.

One possible influence for change might be creatives who move into these communities. Will they bring in a more cosmopolitan worldview? There has been some research on the people who are moving back to small towns and rural areas that shows many are in creative occupations and that they move back to be closer to their families, to enjoy a slower pace of life, and to live in a place where social ties and engagement are more important. 13 They maybe bringing their creative and entrepreneurial talents into their suburban and rural cities, but they are not there to create a mini Midtown Manhattan or a mini downtown San Francisco.

On the other hand, if the incoming creatives are largely young, not nested adults, then there might well be a demand for apartment units. However, brain gain when it emerges in these cities, to date, has brought in more families than singles.

ENDNOTES

1) These cities were selected based on data from: U.S. Census Bureau, Governments Division, Government Organization, Table 7: Subcounty General-Purpose Governments by Population-Size Group and State. Census of Governments (2007).

2) Two of the most successful “redos” are Uptown Charlotte and the Lower Manhattan CBD.

3) Eugenie Birch, “Who lives downtown”, Washington, DC: The Brookings Institution, Metropolitan Policy Program, November 2005, pp 20.

4) Paul R. Levy and Lauren M. Gilchrist, “Downtown Rebirth: Documenting the Live-Work Dynamic in 21st Century U.S. Cities.” Prepared for the International Downtown Association By the Philadelphia Center City District, pp.57

5) Aaron Renn, “SCALING UP: How Superstar Cities Can Grow to New Heights”, Manhattan Institute, Report January 2020, pp. 16, p.1

11) Thanks to Aaron Renn for bringing this to our attention.

12) David A. McGranahan and Timothy R. Wojan, “Recasting the Creative Class to Examine Growth Processes in Rural and Urban Counties”. USDA. https://naldc.nal.usda.gov/download/41989/PDF

Contact: N. David Milder, Editor The ADRR — The American Downtown Revitalization Review 718-805-9507 [email protected]

THE CREATION OF THE AMERICAN DOWNTOWN REVITALIZATION REVIEW (THE ADRR)

There currently is no real professional journal for the downtown revitalization field. For many years, that has been strongly lamented by many of the field’s best thinkers. To remedy that situation, a band of accomplished downtown revitalization professionals are creating The ADRR. It will be a free online publication, appearing four times each year. The target date for the debut issue is now set for the June 1-15, 2020 timeframe, with the second issue aimed for the Sept 7-14, 2020 timeframe.

This ADRR is intended to be a lean and mean operation, based totally on the availability of free online resources and the time, energy and elan contributed by its authors, advisory and editorial board members, and its editor.

How to Subscribe to The ADRR

Those interested can now visit The ADRR’s website, www.theadrr.com , where, on the home page, they can sign up to become subscribers. This enrollment places the subscriber on a MailChimp mailing list so that they can receive New Issue Alerts (see below).

How Issues of The ADRR Will Be Distributed.

New Issue Alerts, containing the Tables of Contents of issues and links to their downloadable pdfs of articles are sent to subscribers via a MailChimp email blast and posted to the ADRR’s website. Each issue’s pdf files initially will be stored in a folder in ND Milder’s Dropbox account from which they can be downloaded. Subscribers can download only those articles they want to read and whenever they want to read them. The ADRR also can be found via Google searches.

The Content We Are Aiming For. Only manuscripts about major downtown needs, issues and trends will be considered for publication. They will be thought pieces and not just reports about a downtown’s programs and policies that its leaders want to brag about. Articles must have broad salience and their recommendations broad applicability within the field. The “voice” of The ADRR will be anti-puff, and very factual, evidence driven, though not dully academic. Discussions of problems and failures will be considered as relevant as success stories if, as so often is the case, something substantial can be learned from them. The ADRR will not avoid controversial issues.

Also, the focus of The ADRR will not be overwhelmingly on our largest most urban downtowns, but also provide a lot of content and relevant assistance to those in our small and medium sized communities, be they in suburban or rural areas.

Who Will Write the Articles?

Hopefully, they will be from people in a broad range of occupations – downtown managers and leaders, municipal officials, academics, developers, landlords, businesspeople, consultants, etc. — who have significant downtown related knowledge and experience.

Curated Articles and Wildflowers. Initially, the ADRR will solicit articles to prime the content pump. Once The ADRR is up and running some articles will continue to be solicited on topics deemed a high priority by the editorial board members. Each board member can select a topic to curate an article on and seek the author(s) to write them. However, there still will be a continual traditional general call for submissions (wildflowers) focused on subjects selected by their authors. All submissions, curated or wildflower, must demonstrate sufficient merit to warrant publication in The ADRR. All submitted articles will be reviewed by board members. We hope to see many submissions!

Article Length and Author Responsibilities.

There will be short reads and long reads. Articles of 1,500 to 5,000 words will be considered. Multi-part articles of exceptional merit and salience will also be considered. What counts is their quality, not their length. Authors must have their articles thoroughly proofread prior to submission. Poorly proofed manuscripts will be rejected. Guidelines for submissions may be found on The ADRR website.

Publication Schedule:

Published four times per year, with a minimum of 5 articles in each issue. Given that this is an online publication, from a production perspective, the number and length of the articles is not a particular problem. However, from an editorial and content management perspective, the number of articles and their lengths can quickly become burdensome.

How It Will Be Organized.

The ADRR will be published by an informal group for its first year, with no person or group having ownership.

Editor. During the ADRR’s first year, N. David Milder has volunteered to serve as its editor.

The Advisory/Editorial Board :

Jerome Barth, Fifth Avenue Association

Michael J Berne, MJB Consulting

Laurel Brown, UpIncoming Ventures

Katherine Correll, Downtown Colorado, Inc.

Dave Feehan, Civitas Consulting

Bob Goldsmith, Downtown NJ, and Greenbaum Rowe

Stephen Goldsmith, Center for the Living City

Nicholas Kalogeresis, The Lakota Group

Kris Larson, Hollywood Property Owners Alliance.

Paul R. Levy, Center City District, Philadelphia

Beth Anne Macdonald, Commercial District Services

Andrew M. Manshel, author

N. David Milder, DANTH, Inc

John Shapiro, Pratt Institute

Norman Walzer, Northern Illinois University

Articles in our first issue that will be published in June 2020

Michael Berne, MJB Consulting, Working Title, ” Bringing Downtown Retail Back After COVID-19”

Roberta Brandes Gratz, “Malls of Culture.”

Andrew M. Manshel, “Is ED Really a Problem?”

N. David Milder, DANTH, Inc., “Developing a New Approach to Downtown Market Research Projects – Part 1.”

Aaron M. Renn, Heartland Intelligence, “Bus vs. Light Rail.”

Michael Stumpf, Place Dynamics, “Using Cellphone Data to Identify Downtown User Sheds”.

The Spotlight: “Keeping Our Small Merchants Open Through the COVID-19 Crisis”

Katherine Correll, Downtown Colorado, Inc.

David Feehan, Civitas Consulting

Isaac Kremer, Metuchen Downtown Alliance

Errin Welty, Wisconsin Economic Development Corporation.

In October of 2017, I posted the above referenced White Paper that outlined my thoughts about how the construction of economic development strategies for smaller communities, especially those in rural areas, should be approached (1). Since then, two data-related findings have come to my attention that have caused me to review some of the arguments I presented in that paper:

I argued in the White Paper, reflecting conventional wisdom among economic development experts, that the lack of jobs was seen as an important constraint on the ability of small rural communities to prosper and retain their populations, especially their Millennials. My recommendations were to try to improve the ability of residents to earn more money and to recruit new residents who would not need new jobs because they were retired and financially comfortable, could bring their jobs with them, or could create their own jobs. However, today, many rural counties, and probably the small towns within them, are sharing in the relatively low unemployment rates, under 5%, that are to be found across the nation. Do small towns in these counties then still need to enhance the earning power of their residents? Does my White Paper’s analysis on this point still stand or need revision?

A major thrust of my argument in the White Paper was that smaller communities should not focus their economic development efforts on chasing after employers who might bring lots new jobs to the communities because they are hard to recruit and relatively few of their residents would get the jobs (most would go to outsiders). Instead, I strongly suggested that primary strategic focus should instead be placed on their resident “contingent entrepreneurs” who are in relatively insecure employment situations and might constitute 30% to 40% of their workforces. The strategic approach I suggested was in essence an attempt to retain and expand these micro businesses. However, the findings of a Bureau of Labor Statistics (BLS) report released in June of 2018 suggest that my estimate of “contingent entrepreneurs” was far too high. Again, does my White Paper’s analysis on this point still stand or need revision?

County Unemployment Rates: A Look at Wisconsin, New York, and South Dakota

Low county unemployment rates came to my attention as I was going over some data about a rural small town in WI. Looking at five distinct years of unemployment data for its county (Grant County, see table), except for the time around the Great Recession in 2010, its unemployment rate was 4.3% or lower, and its rate in April of 2018 was just 2.4%. That was even lower than its 2.9% rate back in 2000. Economists have generally accepted unemployment rates around 5% as normal (2). According to that benchmark, Grant County’s unemployment rates have usually been normal or even lower than normal.

This question then arose: is Grant County an outlier or are rural counties in WI generally experiencing relatively low unemployment rates?

Using a list of WI’s rural and urban counties, I looked at their unemployment rates in April of 2018 (see above table). Yes, the average 3.6% rate among the 46 rural counties is higher than the 3.3% average for all 72 counties and the average 2.7% rate for the 26 urban counties, but the really important point is that the rate for the rural counties was just 3.6%. Moreover, the median unemployment rate for the rural counties was 3.25%, which means that 50% of these counties had rates lower than 3.25%.

Then the question for me became: Is the situation in Wisconsin an outlier? Given time and resource constraints, I decided to look at the counties in New York and South Dakota, two states quite different in character from WI and from each other. NY has an economy dominated by a huge metropolitan area around NYC. Its upstate manufacturing and agricultural industries (e.g., milk) were facing problems long before the advent of the Great Recession. The state also has many sizeable cities besides NYC such as Buffalo, Rochester, Syracuse, Albany, Schenectady, Utica, Troy and Binghamton. Many are doing poorly. For instance, Syracuse has the 13th highest poverty rate among cities in the US. South Dakota is more sparsely populated, less industrialized and more rural that NY or WI.

The average unemployment rate for NY’s 27 rural counties, 5.9%, is higher than the average for all of the state’s counties, 4.6%, and for its urban counties, 3.6%. It also is 63% higher than the rate for WI’s rural counties. However, it is just 0.9% above the 5% benchmark for normalcy. The unemployment rate for SD’s rural counties was 4.2%, below the 5% benchmark and not that much above the 3.9% rate of the state’s urban districts.

The results from these three states suggest that the lack of jobs is not currently a major economic problem for rural areas in many states.

What, then, are the major economic problems in these counties? One is nominal population growth. As a recent study from the Pew Research Center stated: “…rural counties have made only minimal (population) gains since 2000 as the number of people leaving for urban or suburban areas has outpaced the number moving in.” Also, its survey found that rural residents were less likely to want to move to a new community and more likely to live near a family member.(3).

Another can be seen by looking, again at Grant County. Although Pew found its population had grown about 1% between 2000 and 2016, a recent study by the National Low Income Housing Coalition reported that an hourly wage of about $13.25 is required in that county to afford renting a 2-bedroom apartment at a Fair Market Rate, while the estimated average hourly wage of renters is only about $9.68 (4). That means that 26.9% of the Fair Market Rent is unaffordable for the average renters. In turn, that underscores another important point that is part of the conventional wisdom among economic development experts: rural areas need more than just jobs, they need well-paying jobs, one that provide at least living wages. A factor that adds to the issue’s complexity is that that living wages are not defined just by market forces, but also by the characteristics of the households involved. The table below shows what a living wage would be for various types of households in Grant County (5). What also pops out from that table is just how much more income households with children require.

This table is From the Out of Reach 2018 report

It seems that rural residents are willing to cope with a high degree of financial stress to stay in a rural area and close to their families. For some, that stress or perhaps the fear of that stress, reaches the point where they decide to leave.

My White Paper addressed the adequately paying jobs issue in a number of ways. It saw the creation of Small Town Entrepreneurial Environments (STEEs) as a way to:

Help contingent entrepreneurs to find more and better paying work opportunities or assignments in local and larger market areas and to then help prepare these workers to win and successfully complete them.

Stimulate and enable local retailers to implement an omni-channel marketing strategy that can penetrate larger market areas.

Stimulate entrepreneurs with no employees to not only increase their revenues, but also expand and hire workers.

Help local residents identify remote work opportunities and, if they need it, to steer them to the types of training those job opportunities required.

Create an attractive entrepreneurial environment that could attract more capable contingent entrepreneurs and small business operators who prefer living in small towns with high quality of life characteristics, but now reside in urban or suburban locations.

STEEs can still usefully perform these needed functions even when local county unemployment rates are relatively low, both historically or compared to urban counties. Though more people may be employed, many of those with jobs may need and want help to find better paying employment.

The strategy of recruiting firms that will bring lots of jobs to small rural towns does not mean either that a) substantial numbers of those jobs will go to local residents or b) that those jobs will be well-paying, as many small towns have learned from the Walmart and Amazon distribution centers that opened in them. Indeed, many of the firms that seek rural locations do so because they are looking for lower labor costs.

So far, nationally, our resurgent economy has substantially reduced unemployment, but to date it has not significantly increased the incomes of many of our households, especially those with wage earners in non-supervisory positions or in rural areas. Until that does happen, STEEs can be of considerable value.

It seems to me, then, that relatively low to normal unemployment rates in rural counties do not diminish the relevancy or the need for the kind of strategic approach I outlined in my White Paper.

Also, in many states, such as WI, their rural economies are tied to both agriculture and manufacturing. Manufacturing, which tends to be cyclical, has been doing well in recent years. An eventual cyclical downturn or increased robotization may again increase rural unemployment, again worsening rural economic conditions.

The Number of Contingent Entrepreneurs and Their Importance.

At the heart of the strategic approach I argued for in my White Paper were the residents of smaller towns who were, in the BLS’s vocabulary, engaged in contingent and alternative employment arrangements and whom I labeled contingent entrepreneurs. The bullet points below present the reasons why I thought they were so strategically important:

“In these small towns, increasing portions of their workforces are contingent/non-employer business operators. This is part of a larger national trend: the growth of contingent workers, who now account for 30%- 40% of our national workforce. How will they be helped by the attraction of a large employer to their town? Or would the money spent on attracting the large employer have larger local impacts if it were spent instead on them?”

“There are a number of definitions of contingent workers and estimates of their number consequently vary between 30% and 40% of our nation’s workforce. One definition is: ‘Contingent workers are defined as freelancers, independent contractors, consultants, or other outsourced and non- permanent workers who are hired on a per-project basis’. Whether nonemployer businesses are included is not clear for some definitions, while they seem to be either explicitly included in other definitions or implied in still others. In any case, they are perhaps best thought of as entrepreneurs operating micro-businesses – and perhaps we should be calling them contingent entrepreneurs because it is a more fitting name.”

“I would argue that, strategically, these contingent entrepreneurs are extremely important in our smaller communities. They represent a large portion, possibly 30% to 40%, of the residential workforce. Contingent entrepreneurs usually include those in both blue and white- collar occupations. The number of resident contingent entrepreneurs will greatly outnumber the number of jobs that any big employer lured to the town is likely to provide to local residents – or even those attracted to the region.”

“Some contingent entrepreneurs are doing well, while others are doing poorly. If a small town’s resident contingent entrepreneurs are doing poorly, then that town’s economy will very probably also be suffering, even if a big employer has also been lured into the community. Flailing contingents are more likely to need financial assistance from public and nonprofit sources. They are also more likely to move to other climes that offer better employment opportunities. On the other hand, if the town’s contingent workforce is prospering, then the town’s residential units are likely to be occupied and improved, its shops and eateries busy and its playing fields and cinemas filled. The contingents may also grow and develop start-ups that do employ workers.”

My reporting that these contingent entrepreneurs may account for 30% to 40% of the local workforce was based on these numbers being presented in numerous reputable publications since 2010. For example:

In 2010, the Intuit 2020 Report stated that: “Today, roughly 25-30 percent of the U.S. workforce is contingent, and more than 80 percent of large corporations plan to substantially increase their use of a flexible workforce in coming years” (6).

In 2015, the U.S. Government Accountability Office (GAO), responding to Sen. Kirsten Gillibrand, looked into the contingent workforce and its size, characteristics, earnings, and benefits. It found that: ”The size of the contingent workforce can range from less than 5 percent to more than a third of the total employed labor force, depending on widely-varying definitions of contingent work” (7).

An article in Quartz in 2017 cited a 2014 survey done for the Freelancers Union that found that “there are 53 million people doing freelance work in the US – 34% of the national workforce” (8).

As can be seen in the above table, the recently published BLS study results indicate that those engaged in contingent and alternative employment arrangements only account for between 11.4% to 11.9% of our national workforce. The difference between 11% and 30% to 40% is obviously very significant numerically. But, is it significant analytically or from a strategic viewpoint?

First, let me acknowledge my respect and admiration for the BLS’s surveys as I have stated publicly on several previous occasions. However, the GAO’s 2015 report made a very critical point that must be kept in mind when considering the BLS’s findings: estimates of contingent workers and those in alternative employment arrangements differ because of differences in how those workers are defined and the data sets that are used to study them. It may be claimed that the BLS’s definitions are particularly stringent and therefore limiting. For example, one of the analyses in the GAO report estimates that 16.2% of the workforce are “standard part-time workers” and part of the contingent workforce. These workers are not included in the BLS estimates. Moreover, the BLS only looked at primary jobs, so its sample does not include second jobs, be they fulltime or part-time. The latter would exclude, for example:

The arts work of many artists who need a fulltime non-arts job to support themselves and their families, but whose artistic activities constitute part-time jobs and what they want to do fulltime. Or the person who has a fulltime job as a professional planner, but part-time employment as a real estate developer. Or a fulltime university professor who also owns and manages 10 rental apartments.

Workers whose fulltime jobs cannot cover their household’s financial needs and who also have one or more part-time jobs to fill the gap.

Lastly, BLS excluded jobs associated with the gig economy e.g., those with Uber, Lyft, Taskrabbit, AirBNB, etc. from their survey.

In my judgement the BLS estimates should be taken as a very solid minimum estimate of the contingent and alternative arrangements workforce, with the exact number being treated as not knowable at this point in time because of a lack of consensus about how the subject group should be defined. Moreover, I would argue that the minimal BLS numbers are sufficiently large to merit considerable strategic consideration – and that, not the “true” number of contingents, is the critical question. My White Paper needs to be amended to include these points and to somewhat deemphasize the estimates of 30% to 40%. Nevertheless, the critiques of the BLS’s definitions of contingent and alternative work arrangements that followed its recent report combined with the prior research findings produced by very reputable investigators strongly hint that their true number of these workers may well be as high as 30% or so.

The recent BLS report also sparked a debate about the so-called gig economy and the impacts of firms like Uber and Lyft. However, the argument in my White Paper was quite independent of any analysis of, or advocacy for, a gig economy. My concern was: rather than chasing corporations that supposedly will provide lots of jobs, what assets can small towns best leverage to increase the earnings power of local residents? The folks that fell into my “contingent entrepreneur” category had two attributes that might be leveraged:

Many of them were indeed entrepreneurs, whether or not they were incorporated or working fulltime. They incurred considerable risk and had to compete for and win opportunities to earn money on a relatively recurrent basis. If an effective entrepreneurial environment (a STEE) could be built up around them, they might become more successful financially and able to compete in larger market areas. They might also create start-ups that would hire employees. My concern was about their retention and growth: how they could be retained in their communities and how they could earn higher incomes.

Many of them are vulnerable, with low incomes, no benefits and unhappy with their uncertain contingent employment situations. As the table below shows – using BLS data – they prefer traditional jobs. Lower unemployment rates may mean that more of these workers have found steady, more secure fulltime jobs, though their wages may not be at desired levels. The strong information brokerage and networking functions of an effective STEE would be likely to at least help some others to find fulltime and possibly better paying jobs. Some of those jobs might be remote ones.

The table below presents data for a town in the Midwest with population of about 3,900 that is located in a designated rural county. Let’s see how these data can help answer two questions:

Are there contingent entrepreneurs to warrant a program to develop a STEE in this community’s downtown?

Are there enough of them to use in marketing program to recruit more contingent entrepreneurs to live and work in this community?

To help answer the first question, let’s also consider the fact, mentioned in my White Paper, that relatively large firms moving into this community are most likely to average about 50 new job opportunities and the vast majority of them will not go to local residents. The table below shows how many residents of Town X would get jobs at various capture rates. Which is more likely to serve the needs of Town X’s residents a) a program to help its contingent entrepreneurs become more successful or b) a recruitment program aimed at bringing in more employers who can provide on average 50 jobs?

Extrapolating from the BLS data, in the above table on Town X, I conservatively estimate that its contingent entrepreneurs number between 235 to 245 of its residents. Using On-the -Map and other data from the Census Bureau, the table presents an estimate of 80 people with fulltime jobs who work at home and 74 residents who are fulltime self-employed but not incorporated. About seven of those working at home may have remote jobs. Most of these folks are likely to quickly learn about a STEE creation program. How many would then use it now cannot be estimated. Nor can how many will benefit from it. However, activities such as social networking events at local bars or restaurants and distributing information about online freelancer job marts and remote job marts can be done with relative ease and at relatively low-cost.

The chasing companies with jobs strategy has the following advantages:

Possible increased tax revenues

Possible new jobs for residents, with their number being uncertain and may be zero.

The disadvantages are far more numerous:

The odds of a small town recruiting such a job-rich company are relatively low.

The cost of an effective program is likely to be significant and its successes, if any, will probably take a good deal of time to achieve.

Local residents are unlikely to either know or “feel” the recruitment program unless firms are attracted, and new jobs are offered.

In Town X, according to On the Map data, 29% of those who work in that town also live there. If it attracts one firm that brings 50 new jobs, about 15 town residents probably will get them. For more residents to benefit more firms with jobs must be recruited. If three firms were recruited – quite an achievement for a small town — then about 45 residents might benefit.

A significant probability that the jobs offered will not be well-paying.

The town may have to offer incentives to the new firm(s) in the form of tax reductions, cheap land or infrastructure improvements that adversely impact on municipal finances.

Possible traffic and environmental problems.

There is no certainty of success for either of these programs. Local leaders will have to decide and take a chance based on “the best available information. However, one might argue that communities such as Town X should first try the STEE program because it has the potential for benefiting many more residents and then, if that program fails to meet its goals, to switch to a program aimed at helping the existing employers in town to grow. If local employers are few and/or weak, then the recruitment of outside companies that bring in some more jobs for residents may make sense.

The 80 people in Town X who work at home are enough to help develop a quality of life recruitment program aimed at skilled people who will either bring their jobs with them or create their jobs or create new companies that will have employees. There are enough to populate meeting places and events so that a STEE would have a real tangible presence. Their public endorsements of the quality of life in Town X as well as the benefits of the STEE can be strong marketing tools. Their meetings with prospects and becoming “buddies” with those newly arrived also can be very powerful recruitment tools.

There is broad consensus among economic development professionals that retention and expansion is the most cost effective meta strategy. The strategic approach outlined in my White Paper essentially applies it to the micro businesses of a small town’s contingent entrepreneurs. David Carlson, the administrator of the city of Lancaster, WI, argues that, viewed as a collective group, they are analogous to being the town’s largest employer. He then asks: “How much time would you spend working with them to keep them a growing business?”

4) National Low Income Housing Coalition. “Out of Reach 2018,” p.265. http://nlihc.org/oor

5) Ibid. p. 265

6) “Intuit 2020 Report: Twenty Trends That Will Shape the Next Decade.” P.20. October 2010. https://http-download.intuit.com/http.intuit/CMO/intuit/futureofsmallbusiness/intuit_2020_report.pdf

Introduction. Within the economic development community considerable attention has been focused on young, hip knowledge workers and artists. These young hipsters are part of what Richard Florida has termed the Creative Class. Nationally, they have been drawn in recent years to very dense urban areas that they have helped revitalize, from both residential and business perspectives. It is for these reasons that many economic development organization (EDO) leaders have based their revitalization strategies and business marketing programs on the attraction and growth of these “young creatives.”

However, Florida’s definition of the creative class is in terms of occupations, not age. The occupations Florida uses to define the creative class are from the Standard Occupational Classification (SOC):

Super Creative Core: Computer & mathematical; life, physical & social science; architecture and engineering; education, training and library; arts, design, entertainment, sports, media

Going unnoticed –as is probably the case in many of our nation’s large metro areas – is the fact that the heavily suburban counties in Northern NJ also have a lot of workers in these creative class occupations. For example, in 2010, Bergen County had 148,150; Middlesex 141,550; Mercer 112,050; Monmouth 86,350; Somerset 74,600 and Morris 103,500 (see table above). Importantly, many creatives also live in these counties: e.g., in 20011 the numbers of resident creatives were: Bergen 196,892, Middlesex 163,910, Mercer 74,541, Monmouth 125,545, Somerset 80,624 and Morris 120,035. As a result of career stages and geographic location, these “suburban creatives” are older, more likely to have families, have higher earnings and higher net worths, and live in single-family homes than the urban hipsters. Moreover, the suburban creatives are equally, if not more, creative and entrepreneurial. Significantly, they do not have to be attracted to these counties — they are already there. They account for a significant part of the healthy and very desirable residential areas in these counties. Also, the downtowns in these counties that have been able to respond to the suburban creatives’ lifestyles and spending patterns have had successful revitalizations: e.g., Englewood, Red Bank, Ridgewood, Westfield, Morristown, etc.

The presence of the creatives means greater job growth. DANTH’s analysis shows that in the 14 Northern NJ counties that Regional Plan Association includes in the NJ-NY-CT Metropolitan Region, there is a correlation of .81 between the number of creatives in a county’s workforce and the number of new jobs projected between 2010 to 2020 by the state’s Dept. of Labor; the correlation between creatives who live in the counties and their job growth was .92. Looking just at the eight heavily suburban counties of Bergen, Passaic, Middlesex, Mercer, Monmouth, Somerset, Morris and Ocean the respective correlations are .84 and .93. In the 14 counties, there is a strong association, .91, between the number of creatives who live in a county and the number of creatives who are in a county’s workforce.

Economic Strategy and Program Implications. Many EDOs in Northern NJ, be they EDCs, SIDs or municipal or county departments, may want to alter their strategic thinking, marketing and recruitment programs to better leverage their considerable creative manpower assets.

Because economic development in these counties is heavily viewed through retail and office development lenses, one area in which these assets have been minimally leveraged by EDOs is the creation and growth of small businesses operated by creatives. DANTH’s trends analysis suggests that the creatives can be expected to be increasingly entrepreneurial in coming years:

Nationally, the workforce is becoming increasingly composed of “contingent” workers, often creative freelancers. One estimate, by Intuit, sees as much as 40% of 2020’s workforce being contingent. Many young creatives have long followed the freelancer path at the beginning of their careers. Older creatives, who are either laid off or seeking career changes, have also followed this path later in their careers. We can expect more of them to do so in the future.

Many boomers are changing their careers as they enter the pre-retirement 55-64 age group, which has a high rate of entrepreneurialism compared to other age groups

Retired boomers are increasingly starting new careers because they still want to be active and/or they need the income.

The young creatives and their more mature colleagues bring different asset and need sets to starting a business in terms of training, experience, the size and reach of their professional social networks, and their financial resources. Nevertheless, both groups will:

Most probably be inexperienced as entrepreneurs and may need to acquire skills in marketing, bookkeeping, business planning, etc.

Need to raise capital (mostly new firms with employees)

Possibly need to hire employees (the non-freelancers)

Need attractive and convenient places to meet and exchange ideas with other new entrepreneurs and potential clients/customers

Need commercial spaces for their new businesses (the non-home office operations)

Prefer business locations where these needs can be maximized, especially those that are really easy to get to on foot or by car, bus or rail.

The range and depth of these needs will differ mostly not by age, but, as indicated above, between those who are freelancers with no employees and those who are creating firms, usually incorporated, with employees.

Given the relative dispersion in the suburban counties, their stronger downtowns, often their county seats, (e.g., Freehold, Morristown, Somerville, New Brunswick) may be the best geographic locations for meeting these needs. Their existing economic agglomeration offers a density of businesses, government offices, commercial spaces, professional and financial services, restaurants, coffee houses and watering holes in a reasonably walkable area. But, to meet the most pressing needs of the new and budding entrepreneurs, these downtowns may have to develop a more specialized “entrepreneurial infrastructure.” By doing so, the downtown itself becomes a kind of informal incubator/accelerator. Some possible components of such an infrastructure are:

A cadre of technical assistance/entrepreneurship advisors available at nearby colleges and universities or at a SBA Small Business Development Center or at local business consulting firms or through organizations such as SCORE. Helpful would be a mechanism to easily link the entrepreneurs to the types of advisors they need

Besides commercial banks, SBA, and personal investors, these new and developing companies would benefit from having access to other sources of capital such as angel investors, venture capitalists and crowdfunding. Here again, a mechanism to help link the entrepreneurs to these various types of investors would be helpful

Coworker spaces are finding increasing acceptance across the nation. They can be used by freelancers, new companies or small existing companies. They can function as a kind of “business incubator lite” or provide some business acceleration functions for older firms

A full blown business incubator and/or a business accelerator

A variety of relatively small and affordable spaces for a) freelancers who do not want to work at home or in a coworker space and b) firms that either are too large for or also do not want to be in a coworker space. These spaces can be in the downtown or elsewhere within a reasonable drive of the downtown

A mechanism to help link freelancers to project opportunities and where they can get things like health insurance

A permissions and approvals process that is truly timely and affordable for new firms be they startups or new move-ins. Most jurisdictions that think they have a good process upon close inspection are shown to need significant improvements.

(Note: this list is not meant to be exhaustive, but suggestive.)

Some of these components or parts of them may already exist in and near the downtown. Others will have to be created whole or in part.

Some pilot organization is needed to:

Design the downtown’s entrepreneurial infrastructure in terms of its components. This effort should bring into play the major local government agencies having economic development responsibilities, relevant EDCs and any downtown SIDS/BIDs. Most importantly it also should bring to the table major landlords and experienced businesspeople who live and/or work in the county, especially those who are experienced business investors or well networked with those who are

Create an implementation plan that would cover how it would be financed and who would do what

Create an organization to manage this infrastructure or designate an existing organization to do so.

Downtown and County Benefits. Some potential benefits of such a program are:

For a downtown:

Better business retention through the strengthening of some of its small businesses: helping some survive and others to grow in the downtown.

A stronger cadre of freelancers with an increased ability to afford needed downtown goods, services and amenities

Significantly more small businesses wanting to locate in the downtown

Significantly more small businesses wanting to use the downtown’s goods, services and amenities

The development of an image of the downtown as a very business friendly place that is exciting because it is savvy about what small firms need to grow and succeed — and it provides those things

The consequent greater attractiveness of the downtown as a business location to other and even larger firms, with associated impacts on commercial rents, the assessed values of commercial buildings, property taxes, jobs, etc.

For its county:

A program to help increase the success rate of the county’s growing number of county residents who become new entrepreneurs, be they freelancers or incorporated