Contact: N. David Milder, Editor The ADRR — The American Downtown Revitalization Review 718-805-9507 [email protected]

THE CREATION OF THE AMERICAN DOWNTOWN REVITALIZATION REVIEW (THE ADRR)

There currently is no real professional journal for the downtown revitalization field. For many years, that has been strongly lamented by many of the field’s best thinkers. To remedy that situation, a band of accomplished downtown revitalization professionals are creating The ADRR. It will be a free online publication, appearing four times each year. The target date for the debut issue is now set for the June 1-15, 2020 timeframe, with the second issue aimed for the Sept 7-14, 2020 timeframe.

This ADRR is intended to be a lean and mean operation, based totally on the availability of free online resources and the time, energy and elan contributed by its authors, advisory and editorial board members, and its editor.

How to Subscribe to The ADRR

Those interested can now visit The ADRR’s website, www.theadrr.com , where, on the home page, they can sign up to become subscribers. This enrollment places the subscriber on a MailChimp mailing list so that they can receive New Issue Alerts (see below).

How Issues of The ADRR Will Be Distributed.

New Issue Alerts, containing the Tables of Contents of issues and links to their downloadable pdfs of articles are sent to subscribers via a MailChimp email blast and posted to the ADRR’s website. Each issue’s pdf files initially will be stored in a folder in ND Milder’s Dropbox account from which they can be downloaded. Subscribers can download only those articles they want to read and whenever they want to read them. The ADRR also can be found via Google searches.

The Content We Are Aiming For. Only manuscripts about major downtown needs, issues and trends will be considered for publication. They will be thought pieces and not just reports about a downtown’s programs and policies that its leaders want to brag about. Articles must have broad salience and their recommendations broad applicability within the field. The “voice” of The ADRR will be anti-puff, and very factual, evidence driven, though not dully academic. Discussions of problems and failures will be considered as relevant as success stories if, as so often is the case, something substantial can be learned from them. The ADRR will not avoid controversial issues.

Also, the focus of The ADRR will not be overwhelmingly on our largest most urban downtowns, but also provide a lot of content and relevant assistance to those in our small and medium sized communities, be they in suburban or rural areas.

Who Will Write the Articles?

Hopefully, they will be from people in a broad range of occupations – downtown managers and leaders, municipal officials, academics, developers, landlords, businesspeople, consultants, etc. — who have significant downtown related knowledge and experience.

Curated Articles and Wildflowers. Initially, the ADRR will solicit articles to prime the content pump. Once The ADRR is up and running some articles will continue to be solicited on topics deemed a high priority by the editorial board members. Each board member can select a topic to curate an article on and seek the author(s) to write them. However, there still will be a continual traditional general call for submissions (wildflowers) focused on subjects selected by their authors. All submissions, curated or wildflower, must demonstrate sufficient merit to warrant publication in The ADRR. All submitted articles will be reviewed by board members. We hope to see many submissions!

Article Length and Author Responsibilities.

There will be short reads and long reads. Articles of 1,500 to 5,000 words will be considered. Multi-part articles of exceptional merit and salience will also be considered. What counts is their quality, not their length. Authors must have their articles thoroughly proofread prior to submission. Poorly proofed manuscripts will be rejected. Guidelines for submissions may be found on The ADRR website.

Publication Schedule:

Published four times per year, with a minimum of 5 articles in each issue. Given that this is an online publication, from a production perspective, the number and length of the articles is not a particular problem. However, from an editorial and content management perspective, the number of articles and their lengths can quickly become burdensome.

How It Will Be Organized.

The ADRR will be published by an informal group for its first year, with no person or group having ownership.

Editor. During the ADRR’s first year, N. David Milder has volunteered to serve as its editor.

The Advisory/Editorial Board :

Jerome Barth, Fifth Avenue Association

Michael J Berne, MJB Consulting

Laurel Brown, UpIncoming Ventures

Katherine Correll, Downtown Colorado, Inc.

Dave Feehan, Civitas Consulting

Bob Goldsmith, Downtown NJ, and Greenbaum Rowe

Stephen Goldsmith, Center for the Living City

Nicholas Kalogeresis, The Lakota Group

Kris Larson, Hollywood Property Owners Alliance.

Paul R. Levy, Center City District, Philadelphia

Beth Anne Macdonald, Commercial District Services

Andrew M. Manshel, author

N. David Milder, DANTH, Inc

John Shapiro, Pratt Institute

Norman Walzer, Northern Illinois University

Articles in our first issue that will be published in June 2020

Michael Berne, MJB Consulting, Working Title, ” Bringing Downtown Retail Back After COVID-19”

Roberta Brandes Gratz, “Malls of Culture.”

Andrew M. Manshel, “Is ED Really a Problem?”

N. David Milder, DANTH, Inc., “Developing a New Approach to Downtown Market Research Projects – Part 1.”

Aaron M. Renn, Heartland Intelligence, “Bus vs. Light Rail.”

Michael Stumpf, Place Dynamics, “Using Cellphone Data to Identify Downtown User Sheds”.

The Spotlight: “Keeping Our Small Merchants Open Through the COVID-19 Crisis”

Katherine Correll, Downtown Colorado, Inc.

David Feehan, Civitas Consulting

Isaac Kremer, Metuchen Downtown Alliance

Errin Welty, Wisconsin Economic Development Corporation.

A few weeks ago, an article appeared in the Congress for

the New Urbanism’s ( CNU) online journal Public

Square titled “Why downtown retail is coming back ” (1). While the article had some valid and

encouraging points, overall it blurred over a very complex situation in which

retail in different types of downtowns

have different prospects for retail rejuvenation and growth. Most importantly,

there was no discussion of the enormous process of creative destruction that

the retail industry is experiencing, one that promises to continue for many

years to come, and that will strongly structure any rebound. Until we get a

better handle on what the new retail industry will look like we cannot get a

good notion about what the demand for retail locations and spaces will be.

Along that line of thought, the article also ignored the facts that any

comeback must be limited when the demand for retail space by national chains

has had a precipitous decline and 45% of the nation’s household GAFO (general

merchandise, apparel, furniture

and home furnishings, other miscellaneous retail) expenditures

are now being captured by online retailers.

The Public Square article makes much about increased retailer interest in “inner cities,” but this trend is anything but new. Major retailers have long been interested in and placed their stores in some types of dense urban locations. For example, by 1985, a ULI study was reporting a resurgence in downtown retailing propelled by growing CBD employment, an increasing appreciation of urban lifestyles, and a dramatic decline in the number of easy suburban retail project opportunities (2). They even have been going into highly ethnic downtowns since the late 1990s and early 2000s as evidenced by their presence in the outer borough downtowns of Jamaica Center, Fordham Road and Downtown Brooklyn in NYC. The article also failed to note that a whole lot of the major retail that is going into our inner cities is not going into their downtowns, but into large self-contained, car-oriented shopping centers that compete with the downtowns.

This raises two critical questions regarding the inner cities that

are very hard to now answer:

When the overall future demand for

retail space is very likely to be far lower than in the past, will inner city

locations really be getting substantially more retail stores located in them?

How many of those new inner city

retail stores will be locating in the inner city downtowns?

As for the retail chains, we know from past experience, their expressed interest

in locations often is not a good indicator

of where their stores will open.

The article also failed to note that most of our downtowns are in

small communities that always had few if any national chains– and that is unlikely

to change in the future. Nor did it discuss the prospects of the small

independent retailers these small downtowns must rely on.

Yes, it can be argued that new stores are opening, and downtown

retailing will not disappear. However,

since it is undergoing very significant changes in magnitude and operational

characteristics, it is still far too early to make any real sense of claims

that it is coming back.

UNDERSTANDING THE CREATIVE DESTRUCTION OF THE RETAIL

INDUSTRY UNLEASED BY THE GREAT RECESSION

What

we have been witnessing in the retail industry is not the oft mentioned retail

apocalypse, but a classic example, at the level of a whole industry, of what

Joseph Schumpeter called the process of

creative destruction — the “process of industrial mutation that

incessantly revolutionizes the economic structure from within, incessantly

destroying the old one, incessantly creating a new one.” While the media,

in its reporting on the retail apocalypse, has focused its attention on the

destruction, far less attention has been paid to the creation of a new,

vibrant and stronger retail industry, but one that may well require far fewer

and smaller brick and mortar retail spaces. That would mean far fewer and

smaller retail tenants for our downtowns.

The

Industry’s Latent Problems. Prior to the Great Recession, the retail industry was largely

ignorant of the truly bad shape it was in:

As Elizabeth Warren’s book, The Two Income Trap, showed several years before the Great Recession, many middle income households were being financially squeezed by stagnant income growth and quickly rising costs for housing, healthcare, childcare, transportation, and education. Their retail spending was often sustained by home-based loans and/or racking up large credit card debt. The Great Recession turned these households into today’s deliberate consumers who are more cautious about their spending, much more value oriented, and demanding of bargain prices. Gone are the middle income shoppers who “traded up” prior to the Great Recession.

In 2009, a team at McKinsey predicted that by 2011, the internet would be involved – i.e., play some role – in 45% of all retail purchases made in the USA (3). The vast majority of the retail chains seemed ignorant of that already well established trend and did not have very robust online presences, much less viable omnichannel marketing strategies. The shock and hurt the Great Recession threw at so many retail chains, the resulting consumer search for value, low prices and convenience, and the emergence of the “to the internet born” millennials, all led to a growing participation in internet shopping.

Far too many of the retail chains were very badly managed and, of course, their leaders never owned up to that fact. Forever 21’s recent going into Chapter 11 is a classic example of this, see https://www.nytimes.com/2019/09/29/business/forever-21-bankruptcy.html . Unfortunately, too many observers of the industry did not either. The problems proved to be myriad. Worst of all were ill conceived growth strategies based simply on opening more stores. Abetting that problem was a surprising ineptitude in decision-making about where to open new stores, how large they should be, and how close they should be to a chain’s other stores. Too often locational decisions were made not by rigorous analysis, but by following where other retailers were locating, especially their favored co-tenants. The old axiom that retail chains are like sheep — they like to herd — was all too true. The net result was that the chains had too many stores that were also probably too large, and too often in less than desirable locations. Many chains were also burdened by carrying too much debt, especially when they were bought out by financial firms seeking to maximize how much money that could extract from the retail operations. These new managers were not merchants, but MBAs trained in financial manipulations. The large debt burdens caused many bankruptcies. In search of profits, corporate managers cut the size and quality of their in-store sales forces, thus substantially diminishing customer service. Then, too, many chains lost contact with their customers by failing to provide the entertaining ambience, convenience, customer service, sizing and merchandise they wanted. Some chains even failed to notice that their customer base was aging out or moving on.

Chain managers began to look more at the value

of the real estate they owned or leased than increasing the profits from retail

sales. Hudson Bay, for example, closed the Lord & Taylor mother store on

Fifth Avenue in Manhattan not because it was losing money, but because of how

much money selling it could generate. This trend continues.

Across the nation, in the years before 2009,

especially in many of our most successful downtowns, be they in big cities or

affluent suburban or tourist communities, many properties with retail spaces in

them were bought for very high bubble-like prices. That meant that retail rents

would have to increase substantially. Moreover, the financing of these deals

often meant that the retail spaces contractually had to be rented to credit

worthy retail chains. When the Great Recession severely struck the retail

industry, these properties and their ability to attract retail tenants were

placed in a very precarious position. The purchase of the “Devil’s Building” at

666 Fifth Avenue in Manhattan was a prime example, but there were so many

others.

While

one can be hopeful that today’s retail chains and those of tomorrow will be far

better managed than those of the past few decades, their past performance

warrants some skepticism about their future behavior. Prudence also suggests

that we can expect them to continue to make many serious errors, especially when

subjected to the very strong pressures created in a process of creative

destruction.

The

Substantially Weakened Demand for Brick and Mortar Retail Locations and Spaces. The Great

Recession brought these problems to a boil and resulted in many well-known

retail chains going out of business, while many others are still fighting to

stay open.

Countless thousands of chain stores have

closed since 2009 – for example, 7,000+ in 2017 and 7,000+ again in the first half of 2019.

GAFO retailers were hardest hit, especially

department stores and specialty apparel chains.

The surviving chains are looking for fewer new

locations, are being far more selective about locations when they do so, and

their new stores are about 25% smaller than those the chains opened in the

past.

There are about 1,350 enclosed malls in the

U.S., but experts believe that only 200 to 400 are needed (4). Most class “B” and “C” malls are doomed to

closure and reuse.

Also, many malls and open air shopping

centers, to stay popular and solvent, are converting retail spaces to other

uses such as entertainment, personal services, food and drink. Some malls are

even adding housing and hotels. According to Costar, between Q1 of 2010 and Q1

of 2019, malls added about 13.9 million SF of entertainment space while open

air centers added about 52.8 million SF of entertainment space (5). Most likely

these additions were done by repurposing prior retail spaces.

There is little reason to believe that similar

trends are not also occurring in a large proportion of our downtowns. For

example, over the past decade, I’ve seen large amounts of former retail space

being leased to pamper niche – hair and

nail salons, spas, gyms, martial arts studios, yoga and Pilates studios, etc. –

and health care operations in downtowns across NY and NJ.

There has also been “vacancy rate creep.” Back

in the 1980s, a rate above 5% signaled cause for some concern and 10% a

problem. Today, a 10% vacancy rate seems to have become accepted as the new OK normal.

A recent 2019 report by Morgan Stanley found

that while “…e-commerce penetration reached 11% of total retail sales at the

end of 2018” that “e-commerce penetration in the GAFO segment” was

now over 45% (6). GAFO retailers are often the ones downtown leaders most want

to recruit.

This huge

capture rate achieved by online merchants plainly indicates that there will be

substantially less need for GAFO brick and mortar spaces. Will rebounding

downtowns, especially those in our inner cities, really be winning the lion’s

share of this reduced demand?

The

Small Merchant Problem. According to Statista: “There were 19,495 incorporated places registered

in the United States in 2018. About 84%, 16,411 of them, had a population under

10,000.” In contrast, only 10 cities had a population of one million or

more and only 310, or about 1.5%, had a population over 100,000 (7). For the

vast majority of these incorporated places, small independent merchants will be

their most likely retail tenants and tenant prospects. Many of these downtowns

have never had a retail chain, while others were able to attract some non-GAFO

chains and, more recently, dollar stores.

As

can be seen in the table above, the very small merchants, those with 0 to 9

employees had the lowest decline in numbers, -7%, between 2007 and 2012, a strong indication

that they were among the least hurt by the Great Recession, though there was

considerable variation by state. Among them was a huge number of nonemployer

firms. Many of them may have stayed open because the owner also had another

job. Among the small merchants, those with 10 to 19 employees probably account for

many of these small towns’ strongest

retailers. They suffered a significantly

higher decline, -15%, a sign they were hurt more by the Great Recession. They

may have been more vulnerable because they were more likely to have had

outstanding loans.

The

vicissitudes these small merchants have faced were quite different than those

faced by the national chains. For one thing, since most of them were not

offering GAFO merchandise, they were less apt to be hurt by the growth of

internet sales. In the years prior to the Great Recession, any small GAFO retailers were likely to have felt

the brunt of competition from big box stores such as Walmart and Home Depot.

Instead, most small town retail businesses were mainly focused on local,

neighborhood type needs such as food and beverages, health and beauty products,

and arts related products. However, in many smaller and less affluent

downtowns, dollar stores appeared and won substantial market share – even from

Walmart.

Small

town primary trade areas are likely to be small geographically and sparsely

populated. If they have under 15,000 people that is too small to support most

independent small GAFO retailers – unless they adopt an omnichannel strategy that also produces

revenue flows from online sales and offsite sales in distant market areas.

A

major challenge for these very small

merchants is the level of local consumer spending, since it directly impacts

the cash flow they are so dependent on. Those in communities where household incomes are hardest hit

will feel the pain most. Those in communities where income and population

growth are stagnant will likewise probably work hard just to tread water. Retailers in small communities with strong household

incomes are more likely to prosper.

Other

major challenges for these small merchants are their skill sets and abilities

to start and maintain a successful business.

By definition, half can be expected to have below average skill sets. According

to BLS data from 2016, about 56.1% of retail startups fail within their first

five years. That means that the smaller downtowns towns dependent on small

merchants can likely expect significant churn with the resulting need to either

recruit or develop new retailers. A possible confounding problem is that

nationally the number of startup firms seems to be diminishing, having fallen

by 19% between 2007 and the first half of 2019 (8). How much this holds true

for small retailers is not now apparent, but if the number of small retail

startups has diminished, that could have important implications for many

smaller downtowns.

The

Green Shoots of the New Retail. On the other hand, there are many signs that brick and mortar

retail will not be completely disappearing, though how many locations and

how much physical space will be required are not now known. Here are some

of the positive signs:

Most Americans still prefer to shop in brick

and mortar stores — 64% according to a

2016 Pew Research Center national survey; 78% also said it’s important to be

able to try a product out in person (9). Several other surveys have over the

years had similar findings. The problem has been that the types of stores

retailers have offered shoppers have not been what many of them wanted! That is

beginning to change. There has been a big increase in retail chain concerns

about better instore experiences and more convenient transactions (purchasing

and deliveries).

Some chains have continued to do well through

these apocalyptic times – off-pricers such as TJ Maxx; dollar stores; grocery store chains such as

Wegmans, Kroger and Aldi, and beauty product stores such as Sephora and Ulta.

Many “old” retailers seem to be learning new

tricks. For example: Best Buy and Target have made notable comebacks; Walmart

has created an impressive internet operation; Kohl’s is experimenting with

smaller stores, bringing in Amazon returns,

and putting Aldi groceries inside its stores, and Chico’s has reportedly found new online

marketing legs.

More retailers are realizing the importance of

customer relationships and how convenience and instore experience can help

build them.

While chain stores have been closing, they

also have been opening, if at a lower rate. Old Navy, for example, plans to

double its store count and penetrate smaller communities.

Internet birthed retailers are opening brick

and mortar stores. They need them to be profitable! It remains to be seen how

many stores they will open. Many of them reduce their space needs and costs by

not keeping merchandise inventories onsite. Many of them like affluent downtown

and neighborhood shopping district locations.

Most importantly, retailers are now avidly

adopting omnichannel marketing strategies that see both brick and mortar stores

and their internet assets as related

ways of connecting to their customers — and often on the same transaction. For

example, it is becoming increasingly popular for shoppers to make a purchase on

a retailers website and then pick it up at the retailer’s nearby physical

store. Retailers are finding that physical stores can stimulate visits to their

websites and conversely that websites can stimulate visits and sales in their

brick and mortar stores.

Retailers are increasingly finding that besides

making sales, physical stores can play many other valuable roles related to

interfacing with shoppers, e.g., being places to pick up purchases,

experience/try out merchandise or

receive pampering amounts of customer service. Their annual sales consequently

may be a poor indication of their true value to the retail chain – or to the

landlords of their leased retail spaces.

Experimentation with smaller stores has been

going on for many years now. Walmart famously tried to do so in some rural

areas, and retreated. Now, a number of other chains are trying out smaller

stores that allow them to enter dense urban markets where their larger formats

cannot fit and/or would create traffic and/or political problems. Target has

been the most visible. The argument can be made that this is an extremely

important experiment for downtown retail growth. If the chains can learn

how to do the smaller formats successfully more will fit not only into dense urban

downtowns, but also into suburban and some rural downtowns. The key to their success

may be how they use the internet and AI

or AR to augment the smaller selections of merchandise they can offer in the

smaller spaces.

As I have noted in an article in the IEDC’s

Economic Development Journal, there is a definite trend in some rural and

suburban communities for new residents, drawn by the area’s quality of life

assets, to open new retail shops (10). In several instances, these shops and

eateries have become some of the best in the downtown. Quite often, those QofL

retailers have been facilitated by the market shares yielded by the department

stores and specialty retail chains that closed in failing nearby malls. It

should be remembered however, that many of these closing retail operations had

well below average market shares – that’s why they failed – and what they gave

up was also prone to being captured to varying degrees by the remaining retail

chains and online merchants.

LOOKING

AT SOME DIFFERENT TYPES OF DOWNTOWNS

Trying

to present a full typology of downtowns would require an arduous and

complicated effort that would likely

divert attention from the main subject of this article. Additionally, just

looking at a few examples will amply serve the purpose of demonstrating different

retail outcomes.

Urban

Downtowns and Commercial Districts. One well-known retail expert was quoted in the Public Square

article as arguing that : “Retailers have saturated the suburbs and the next

underserved market is the inner cities. And they are also thinking that it will

be a trend and growth market.” I found that use of the term inner city somewhat

confounding since I have heard it used overwhelmingly to refer to the core poor

parts of a large city that are usually heavily populated by “minority” groups,

while I think the expert was really using it as a broader synonym for “dense

urban areas”. Within dense urban areas

several different types of retail districts can be found if categorized just by number of stores and shopper affluence –

there is not just one type of inner city retail, district. Here again, to

maintain some brevity, I will focus on a select few. I will look at Manhattan and other NYC retail districts simply

because of the ease of finding relevant

data because of my past research on them.

The Crème de la Crème. This is undeniable: in our major cities, for countless decades there have been major CBD retail corridors that have attracted hordes of trophy retailers– e.g., Fifth Avenue and Madison Avenue in NYC, Newberry and Boylston Streets in Boston; North Michigan Avenue in Chicago ; Rodeo Drive in Beverly Hills, and Walnut Street in Philadelphia. The retail chains show how much they value such locations by not only being there, but by how much they pay to be there. For example, retail rents on the prime part of Fifth Avenue in Manhattan run about $2,871 PSF and about $960 PSF on Madison Avenue – see table above. The retailers often are there as much for the marketing opportunities provided by a “flagship store” as for the actual sales they make. That said, those sales can be huge. Back in 2009, the Apple store on Fifth Avenue reportedly had sales of $350 million, or about $35,000 PSF! Nearby Tiffany reportedly did about $18,000 PSF. (I’ve tried unsuccessfully to confirm these stats. I do not doubt that the sales PSF are very high, but they being that high, I am not sure.)

The

table above is from a report by Cushman & Wakefield on 11 of Manhattan’s

major retail submarkets. Unsurprisingly, Manhattan has tons of retail because

it has a large, affluent population, hordes of people working there and loads

of tourists, especially from abroad, who spend lots of money in retail shops.

The lowest retail asking rent is in the

table is $243 PSF and the average is

$860. It is reasonable to assume that most of the retailers paying such rents

were doing so because they expected commensurate sales revenues and profits. This

shows another basic and perhaps mundane point about our retail chains –they

have long entered urban commercial districts and been prepared to pay very high

rents when they saw a lot of affluent people living, working, playing and

spending in them. The question about retail interest in dense urban

areas has really been about their willingness to enter less affluent inner city

areas.

However, even these affluent submarket areas can have their problems. The Cushman & Wakefield data also show that across these 11 strong submarkets, about 21% of the commercial space is “available”, i.e. vacant or up for lease. In turn, that level of availability suggests that in these strong urban submarkets, something is not quite right. It very probably has little to do with their addressable consumer markets. Most of those consumers have benefited from income inequality, not been hurt by it. More likely are problems associated with the involved real estate properties and their tenants. Some proof of this is that when asked rents have been lowered, the availability rates also went down. There also is a real possibility that there is just too much retail space on the market, even in these posh market areas. It will be very interesting, for example, to see what happens in the 34th Street district after all the new retail space built by Related and Brookfield in and near Hudson Yards is fully activated. Also, greater retail chain entry into urban districts will depend on a lot more than just their desire to do so. It will also depend on local landlords and, as Walmart and Target have learned, the approval of city politicians. Surely, NYC is not the only big city facing such issues. Many of these major city downtowns, for example, have seen the closing or down-sizing of their department stores.

Some of the retailers on Austin Street in Forest Hills, NY

Long Successful Densely Populated Urban Districts. Here in the Borough of Queens, there are two shopping areas that demonstrate that retail chains also have long known about, located in, and succeeded in dense non CBD urban market areas with high expenditure potentials. They are also interesting because they have quite different operational characteristics and customer bases that exemplify what is happening in many of our non-crème de la crème urban commercial districts. Austin Street is a narrow two-lane street that runs parallel to the six- lane Queens Boulevard one block to its north. For about 100 years it has been the shopping area for Forest Hills Gardens and Forest Hills. Since about 1980, it has attracted upper middle income shoppers from an even wider area as such retailers as Gap, Gap for Kids, Banana Republic, Ann Taylor, Benneton, Loft, Nine West, Barnes & Noble, Victoria’s Secret, Aldo and Eddie Bauer decided to locate there– see photos above. Over the years, it has had its ups and downs usually in sync with the general economy. Recently, the B&N closed and one of Target’s “small stores” took its place, and Banana Republic and Ann Taylor have converted to “outlet/ factory” formats. In recent years, more national chains have closed than opened, with retail spaces being replaced mainly by eateries such as Shake Shack, Bare Burger, and high quality Asian restaurants, and personal services such as non-appointment doctors offices and barber shops.

There

are few large commercial spaces on this traditional street, the largest being

the one Target occupies that has about 25,000 SF. Attempts to redevelop

this area to create much larger retail spaces would almost certainly create

a political storm and likely be defeated. If retail chains are to increase

their numbers on Austin Street it will likely be by those able to use value

oriented formats that do not require large spaces, such as the current Ann

Taylor and Banana Republic factory stores. There is no existing space for

another retailer of Target’s size, or a small Whole Foods or a small

Kohls.

Today,

the storefronts constitute a traditional solid line of commercial activity on

both sides of the street for about 0.6 miles. It has a nice scale. It is

walkable, though its relatively narrow sidewalks can quickly seem crowded on

weekends. It can be accessed via four subway lines, the LIRR and several bus

lines, with most shoppers walking or busing there. Parking there is tight both

on-street and off, and not cheap. Some

of its independent retailers have been there for decades. It has some attractive eateries and bars. The

whole package is very much like a successful, walkable suburban downtown and it

attracts some of the borough’s more affluent shoppers who appreciate a non-mall

experience. The core neighborhoods Austin Street serves – Forest Hills

Gardens, Forest Hills and Kew Gardens – were early planned suburbs of Manhattan

and today they maintain many suburban characteristics.

The Austin Street district’s zip code area has 68,733 residents, 61% of whom are white only. The average household income is $101,342, and the median is $76,467. About 38% of the households have annual incomes over $100,000 and they will likely account for a very disproportionate amount of local retail spending. Over 59% of its adult population have a BA degree or higher and 59% are engaged business, management, science and arts occupations. In other words, within walking distance of the retailers on Austin Street are a large bolus of creative people and lots of households with significant spending power.

Rego Park-Elmhurst Shopping District Map

Just about one mile to the west of the Austin Street district, at 63rd Drive, starts another commercial district that runs about 0.7 miles west along Queens Boulevard. See the above map. It straddles two neighborhoods, Rego Park and Elmhurst and its major retailing is a fragmented and dispersed set of shopping centers. Elmhurst is the most linguistically diverse neighborhood in the US. The character of this shopping district and its tenants are quite different from Austin street. It has the Queens Center, an enclosed mall that opened around 1980 and for several decades was one of the top grossing retail centers in the USA on a $/SF basis. It also has some power centers with tenants such as a full-size Target, Best Buy, Costco, Burlington, Marshall’s, Century 21, TJ Maxx, Aldi, and Trader Joe’s. This district is not pedestrian friendly, and its mass transit assets are a couple of second rate local subway stops. But, it’s very car oriented, abutting the very heavily trafficked Long island Expressway (LIE) and Queens Boulevard and it has loads of parking garage space. Regardless of what NYC’s planners and idealists may believe or want, most Queens residents who have cars use them frequently to go shopping at places that are beyond walking distance. This shopping district’s location allows it to tap the many shoppers with cars who live in Queens.

The

Queens Center Mall offerings are those of a middle market mall. For example, it

has Macy’s, JCPenny, Michael Kors, Gap, Victoria’s

Secret and an Apple store. It is in a zip code that has a population of 96,353

– making it equal to a fairly large city — with median and mean household

incomes of $49,098 and $65,321 respectively. About 20% of the households have

annual incomes over $100,000. This shopping district is located in a solidly

middle income residential area and its big box value retailers are aptly

positioned both in their locations and their offerings to tap that market. However,

its car orientation and location next to two highly trafficked roadways means

it also can draw many shoppers from well beyond its zip code.

This

district does not operate in any way that resembles what a well-designed and

well run downtown should be. If this is the model for today’s retail chains to

penetrate our urban areas, then there may well be strong reasons to question

the value of their entry. Over the past decade, for example, some big box operations have

entered Jamaica Center – Marshalls and Home Depot – but observers report that

their shoppers, who mostly arrive by auto,

do not spend much time walking around and shopping in other downtown

stores. it is hard to see how the insertion of power centers or even a mall as magnetic

as the inward-looking Queens Center, would do much to help other nearby downtown

retailers or make the district to appear more vibrant. For example, part of the

reason The Gallery in Center City Philadelphia failed is that it was not very

permeable to pedestrians on Market Street. Fashion District Philadelphia, the heavily

renovated mall that replaced it,

reportedly is far more permeable for pedestrians.

Underserved Inner City Districts. Now let’s look at the inner city downtown and neighborhood districts where large numbers of lower income, non-white populations shop. Over the years, I have done a lot of work in places such as Jamaica Center in Queens; Fordham Road, Norwood and Hunts Point in The Bronx; Downtown Brooklyn; and West New York and Elizabeth in NJ. Since the early 1980s, I’ve heard about these districts being underserved by retailers and on many occasions I, too, made that argument. There is absolutely nothing new in that argument. What I usually found was that:

Local leaders, landlords and a tranche of middle income trade area residents were dissatisfied with the retail offerings as well as the district’s appearance and fear of crime.

Yet, there were numerous shops, fairly normal vacancy rates, and the sidewalks filled with pedestrians during the daytime . After visiting a few of them, one former president of Bloomingdale’s called them “beehives of activity.”

Over time, the dissatisfaction increased as the retail shops stopped serving middle income shoppers and focused more on lower income, “ethnic,” and teenage shoppers.

In seeming validation of Michael E. Porter’s famous argument in “The Competitive Advantage of the Inner City,” that dense low income populations in aggregate offered strong market potentials, the inner city retailers who focused on lower income shoppers very often reported strong sales PSF that rivaled those reported for some of Manhattan’s posh shopping corridors (11). Indeed, some were doing so well that they created their own chains that opened stores in inner city downtowns and large commercial centers across the NY-NJ-CT metropolitan region and even in PA.

Trade area analyses of these downtown and large neighborhood shopping districts consistently showed that the number of solidly middle income households were either sizeable or even in the majority, and certainly accounted for most of the retail spending power. For example, the 1987 report I co-authored with Bill Shore on Jamaica Center found that the households in its trade area had a 10% higher average income than those in NYC as a whole (12). In 2002, DANTH looked at the trade area of the Jerome Avenue BID in The Bronx and found the median household income in 2019 dollars was about $76,234 and 22.8% of the households had incomes in 2019 dollars above $109,889. What Porter appears to have missed is the fact that while many and probably most of our inner city commercial districts may be drawing from areas that are indeed heavily “ethnic,” with many lower income people, they also can have large numbers of solidly middle income and even upper middle income households that have most of the spending power.

Nonetheless, the retailers in these inner city districts were targeting the trade areas’ lower income residents and less affluent district visitors. In many instances, the low income segment was targeted by the retailers because they lived in or near the downtown and were its most frequent users. The market research of too many of these retailers was limited to observing the types of people they saw walking by their shop or possible location. More importantly, the retailers very often were making very sizeable profits – Porter did see this possibility –and saw no reason to take the risk of trying to attract their market area’s more affluent shoppers.

Jamaica

Center.

NYC has several outer borough downtowns. Jamaica Center is one of the three in

Queens. It is old, dating back to the colonial days. In 1947, when Macy’s

opened its second branch store in NYC, it was in Jamaica Center. It was long a true, multifunctional downtown. However, by the late 1960s, it

faced a steep decline with white residential and retail flight. In the late 1990s, and especially after

Porter’s article received wide national attention, some of the more sought

after national chains started to look more closely at dense inner city downtowns,

and Jamaica Center was one of them. By 2002, for example, One Jamaica Center, a

450,000SF a mixed-use complex was opened with tenants such as Old Navy, Gap, Bally

Total Fitness, Walgreens, Subway, Dunkin’ Donuts, a 15-screen multiplex theater.

Marshalls, Home Depot,, Footlocker, Petland also have located there. Just

opened are H&M and Burlington Coat Factory. Among those that have come and

gone are Payless, Toys R Us, Kids R Us, The Athlete’s Store – retailers

troubled at the corporate level. Gap is now in another location and using a

factory store format. Jamaica also still has lots of the chains that have long

felt comfortable being in inner city commercials districts such as Fabco, CH

Martin, Conway, Danice, Rainbow, Shoppers World, Young World, GNC, Game Stop,

Jimmy Jazz, Dr Jay’s, and Vim. Target is reportedly may locate in a new mixed

use project and it will be very interesting to see if it is a small store or

one of its larger formats. The smaller Target stores I’ve seen in urban

locations are not in inner city ethnic districts — my experience may be

limited – but in very solid upper-middle-income, non-CBD commercial areas such

as Austin Street or on East Illinois near the lake in Chicago.

The

emergence in Jamaica Center of a cluster of well-known national retailers who

appeal to middle income shoppers looking for value in their purchases is a

process that started many years ago and continues on today. There has not been

any sudden huge gush of retail interest, but a long-term series of stops and

starts that is building a herd of retail sheep that hopefully will reach the

critical size needed to attract more

retail sheep. Notably, this meeting of middle income retail demand is being

done by retailers with value formats – even the specialty apparel retailer, Gap,

is using one. There was normal churn, but no new large influx of retailers

targeting poorer shoppers – those retailers were long there.

Jamaica

Center had several existing large commercial spaces that could be converted for

use by these big box value operations. Among them were old department stores,

an old newspaper building and large former furniture stores. When will the

supply of those large spaces run out? What, if anything, will be done then to create new ones?

Very

importantly, for the first time since the early 1960s, a very substantial

number of new housing units are appearing in Jamaica Center. One might suspect

they will intensify retail chain interest. If so, that points to the strong

possibility that if other inner city downtowns are now enjoying first time or

greatly increased retail chain interest, it may be because they have improved

in important ways that made them more attractive to retailers — and less

because the retailers have suddenly seen the light and are newly interested in

inner cities. Greater interest in downtown Detroit, for example, by retail

chains that are now doing well, would not be surprising given the significant

revitalization that has occurred there in the recent past.

Lessons to learn From the Retail Growth in The Bronx. There are perhaps no better examples of poor ethnic inner city neighborhoods than those found in The Bronx, NY. It has 1.5 million residents, a population density of 32,903/SqMile, the lowest per capita income among NY’s 62 counties, and only about 10% of its population is white only. For decades, the fact that the entire borough was badly understored was widely acknowledged, and largely ignored by retailers and developers. However, in a slow, start and stop manner, retail has been growing in the borough since the opening of the powerful Bay Plaza Shopping Center in the mid 1987, with another burst in the early 2000s and considerable growth since the Great Recession. The table below lists the major shopping centers in the borough and provides some demographic information about them. Since around 2000, well over 3 million SF of new retail space has opened in The Bronx, with over 2 million SF since 2009.

Fordham

Road and The Hub are the two shopping districts with the physical

characteristics most like those of a downtown. They are also in the zip codes

with the greatest population densities and the lowest and third lowest

household incomes. Both have strong subway assets and Fordham Road has an

increasingly used Metro North station next to a large bus transfer point. Both

have comparatively little off street parking and are not that close to a major

highway. However, these two downtown-like districts have attracted a relatively

small portion of the new retail. The Hub

has seen little to no real growth. The 300+ store Fordham Road district has

done better. It remains a beehive of activity well after two major department

stores closed: Alexander’s and Sears. It has attracted a significant number of

national chains: American Eagle Outlet, Best Buy, Claire’s, Footlocker, GameStop,

Gap Outlet, Macy’s Backstage, Marshall’s, Nine West Outlet, Payless, Rainbow,

Sleepy’s, Staples, Starbucks, The Children’s Place, TJ Maxx, Walgreens and

Zale’s. Many of the larger chain tenants – Marshalls, TJ Maxx, Best Buy, and Macy’s

Backstage have gone into the buildings vacated by the department stores. Here,

as in Jamaica Center, large value and outlet retailers are important. There are few if any large retail prone

spaces of say 25,000+ SF available and that is probably constraining the

district’s ability to attract more major retailers.

Most

of the new comparison retail in the borough has gone into the other shopping

centers listed in the table. The characteristic they all share is that they are

car oriented: they sit next to major highways and have lots of off-street

parking.

They plainly are targeting shoppers who are located well beyond the

neighborhoods they are located in. For example, Target is an anchor tenant in three

of them and claims addressable trade area populations of 400,000+. The retailers entering into this paradigmatic

inner city county are showing by their stores how much they nevertheless still

favor self-contained car-oriented shopping centers over downtown-like

locations. To some degree, this may be because of the lack of appropriate

spaces in The Hub and along Fordham Road.

The

Bronx Terminal Market (BTM) is a 913,000 SF retail complex that opened in 2009,

despite the Great Recession, is perhaps the strongest example of the retailers

continued preference for strong highway access locations. It is owned and

operated by the Related Companies, one of the largest real estate

developers/owners in the USA. Its presence in the Bronx more than 10 years

ago certainly demonstrates that the interest of important retail developers and

retail chains in The Bronx is not new. The new Yankee Stadium also opened

in 2009. With the new stadium, political leaders and the Yankee organization

wanted the surrounding area improved. Metro-North put in a new station,

existing subway stations were improved and the BTM was built. Its tenant list

included: Babies R Us, Bed, Bath & Beyond, Best Buy, BJ’s, Burlington, GameStop,

Home Depot, Marshalls, Michael’s, Raymour & Flannigan, and Target. That’s

one powerful retail line up! Those retailers need to draw from a very wide and

densely populated trade area, one that probably goes well beyond the South

Bronx. The BTM’s location right next to I-87 allows such market penetration. Aside

from that asset, the BTM’s location is not a particularly desirable one for

retailers. It is located in a relatively

low-income zip code that has a population density that is far from the highest.

Its strong car orientation indicates

that while it certainly might draw some close by lower income shoppers, its

primary customer base will be middle income shoppers located along the I-87

driveshed.

The

Kingsbridge Broadway Corridor in Zip Code 10463 has attracted three shopping

centers that together total 530,000 SF. The first opened in 20004 and the other

two in 2014 and 2015. They too sit very near an I-87 exit. Their zip code’s

residents are solidly middle oncome and 24% of the households have annual

incomes of $100,000. This corridor is very interesting because retailers there

can tap the close-in Kingsbridge, Riverdale and Inwood neighborhoods. The three

shopping centers have definitely increased the retail choices of local

residents. The distances between these three shopping centers are certainly

walkable, but the way they are built and the setting along Broadway are not

conducive to making such walks. They are not downtown-like and have done little

to stimulate the creation of a walkable shopping district along this section of

Broadway.

The

300,000 SF Throggs Neck Shopping Center that opened in 2014 is in a similar

type of location. It is next to an exit on I-95 and the residents on its zip

code are solidly middle income, with about 23% of the households having annual

incomes of $100,000. The Targets in this and the River Plaza shopping center

both have their main sales areas underground, as does the Costco in Rego Park.

This was done to bypass the zoning aimed by city fathers at deterring the

opening of large big box stores.

The

New Horizons Shopping Center is a supermarket anchored center in a low-income

neighborhood. It was created through the hard work of a terrific neighborhood

organization, the Mid-Bronx Desperados (MBD), that worked with LISC. Today, it

has a Stop & Shop, Auto Zone, TJ Maxx, Footlocker, Petland, Game Stop,

Subway, IHOP and Taco Bell. This is a traditional suburban type, car oriented

shopping center, with shops located in a

sea of parking spaces. It is also very close to the Cross Bronx Expressway. It

is not an urban shopping project with a solid wall of shops on the ground floors of

buildings that abut and open to sidewalks. On the once infamous Charlotte

Street, MBD had previously built ranch style single family residential units.

Their occupants have well-tended backyards, some boats sitting in driveways and

some above-ground swimming pools. Given their MBD origins, both the housing and

the shopping center certainly reflected local aspirations and needs. Residents

in many other dense, low-income, ethnic urban areas may also aspire to more

suburban type retail projects. Because people are less affluent does not

necessarily mean they like downtown or other urban retail environments.

That may prove to be another challenge to inner city downtown retail growth.

The

Bay Plaza Shopping Center and Mall is an example of a large and growing

suburban mall, but one located in the middle one of the most densely populated,

highly “minority” and poor counties in the nation. It is isolated in the geographic arm

fold of two major highways, I-95 and the Hutchinson River Parkway, and only

accessible by car or, with some difficulty, bus. It plainly is targeting middle

income shoppers not only in The Bronx, but also in lower Westchester County. Opened

in 1987, it has grown to over 2 million SF, adding 780,000 SF in 2014. Its tenants

range from traditional department stores (e.g., Macy’s) and specialty retail

chains (e.g., Victoria’s Secret) to the value pricing department stores

(Marshall’s and Saks Off 5th) and retail chains (DSW). Also included

are several regional chains such as Easy Pickins and Jimmy Jazz. Importantly,

they have also attracted retailers who are big hits with teens and young

adults, such as H&M, Forever 21, and Hot Topic. The array of national

retailers in this mall far outshines what The Bronx’s closest approximation to

a downtown, Fordham Road, has to offer.

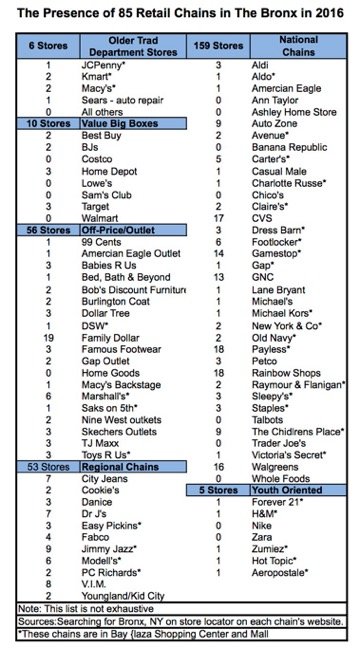

Back in 2016, I compiled a list of 85 national chains and researched how many had locations in The Bronx (13). See the table above. While the list certainly was not exhaustive, the results are hopefully still informative. I found 75 of the identified chains had Bronx locations and together they had a total of 290 stores.

As

might be expected, The Bronx still has not attracted. the likes of Gucci,

Prada, Valentino, Tiffany, Duxiana, Ralph Lauren, etc. They are far, far too

ritzy and more appropriate for Rodeo Drive in Beverly Hills, Midtown Manhattan

or the Americana Shopping Center in Manhasset, NY. Nor is The Bronx attracting,

perhaps thankfully, those like Talbots, Chico’s, Ann Taylor or Banana Republic

– many of these apparel chains still are fighting for survival. Trader Joe’s

and Whole Foods still have stayed away. So have Walmart and its sibling Sam’s

Club – due more to strong political opposition in NYC to Walmart than the

chain’s lack of interest in NYC locations.

The

retail chains that now seem to like the inner city Bronx’s markets the most are those:

Aiming at the lower income and

ethic shoppers: e.g., Family Dollar, Dollar Tree, Dr Jays, Jimmy Jazz, Rainbow

Shops, Vim and City Jeans. Many of them have been around for decades.

With a neighborhood level store

location strategy: e.g., GNC, Walgreens, Payless, GameStop, AutoZone and CVS.

These types of retailers have been locating in ethnic inner city districts

since the mid 1980s.

Targeting middle-income shoppers in either big box, off-price, or factory

outlet formats. Includes Home Depot,

BJs, Best Buy, Target, Burlington Coat, Marshall’s, TJ Maxx, DSW, Gap Outlet,

American Eagle Outlet, Macy’s Backstage, Nine West Outlet, Aldi, Saks Off 5th. These are more likely to have arrived after

2002, but some go back to 1987.

The retailers honed in on the middle class now operate in ways

that recognize its huge number of deliberate consumers who are:

Much more value conscious.

Cautious spenders.

Expect big price discounts from retailers.

SOME

TAKE AWAYS

1.

What national retail chains may do is largely irrelevant for a very large

number of our downtowns that are small. They either never had any chains or

only had a few non-GAFO chains. Their trade areas often are far too sparsely

populated – e.g., probably under 15,000 people –to support small GAFO retailers.

In these small downtowns, the abilities

of local merchants will be a more critical factor than the behaviors of

national retail chains.

2.

Most needed in these small towns are better merchants, through either

recruitment or re-training.

3.

That our inner cities are underserved by retailers has been recognized at least

since the early 1980s. This is not a new situation, nor is the awareness of it.

4.

National retail chains, probably since their inception, have been interested in

prime urban locations where lots of wealthy people lived and played, and they

have been prepared to pay a lot for them. Their locating today near to large new

market rate housing projects, especially if they are expensive, or in a walkable or TOD neighborhood, absolutely

comes as no surprise. What would be a surprise, is if they behaved otherwise.

5. For over 20 years, national retailers have been locating in highly ethnic inner city districts and downtowns, but the levels of their interest have been uneven over time and across places. The questions sparked by the Public Square article are: a) will retailers now locate in our inner cities at a higher rate than before, even though their demand for new retail space has significantly decreased, and b) will those stores be located in our inner city downtowns?

6.

The retail demand of low income shoppers in these inner city districts were

long met by local retailers, who often had lucrative businesses and created

chains targeted to low-income shoppers in similar districts.

7.

Middle income shoppers were the most underserved and complaining inner city

market segment. They were often surprisingly numerous and accounted for a large

proportion of an inner city area’s residential retail expenditure potentials.

8.

National chains that usually targeted middle income shoppers have over the past

20 years increasingly entered inner city districts, targeting, as might be

expected, local middle income shoppers. It is their presence and not the

density of the low-income shoppers that attracts these retailers.

9. The retailers best positioned to capture

middle income shoppers these days are those that feature strong value pricing in either big box,

off-price or factory outlet formats. These are precisely the types of retailers

that are entering densely populated inner city areas.

10.

Many of them require relatively large spaces and are accustomed to being in

very car oriented retail centers. They often are hard to fit into a downtown,

especially if it lacks large retail prone spaces and parking capacity. Consequently,

these retailers may prefer to locate in non-downtown inner city locations, and

downtowns might not benefit so much from any increased retail chain interest in

inner city locations.

11.

The use of smaller formats theoretically could enable more of these chains to

locate in downtowns, but their viability is still being tested and their placement

in ethnic inner city districts now is still uncertain.

12.

Most importantly, the retail industry remains in the midst of a process of

creative destruction that does not promise to end any time soon. As a result, how

much retail space will be needed in the future remains unknown, though it now

looks like it will be considerably less than it was even a few years ago. Also,

still to be clarified, are the uses the retail spaces will be put to, and how that will impact the amount of space needed,

their best locations and costs. These factors all have strong possible

implications for any downtown retail rebound.

13.

Many other factors, besides the interest of the retail chains will determine

how a downtown’s retail will rebound. Among them are: the abilities and

behaviors of retail chains’ managers and local landlords; political, urban

design and environmental issues, the availability of appropriate retail-prone

spaces and ample parking, and, most importantly, where and how local consumers

like to shop.

14.

There are some other interesting types of downtowns that appear to have their own

retail development scenarios these days: downtown creative districts; the lifestyle

mall suburban downtown; the urbanized suburban downtown; the rural regional

commercial center downtowns, and the small rural downtown gems. Unfortunately,

I cannot cover them in this already long article, but I want to acknowledge

their existence.

For many years downtown revitalization experts lamented that large, ethnic downtowns — those with lots of African American and Hispanic shoppers — were being avoided by major retail chains.

That is certainly no longer the case. Here, in New York City, one of the hottest retail locations is along 125th Street in Harlem. Many retail and fast food chains are also occupying important storefronts in the outer borough downtowns such as Jamaica Center in Queens, Downtown Brooklyn and Fordham Road in the Bronx. They are also opening in strong neighborhood shopping districts such as Jerome Avenue in the Bronx and and Corona Plaza in Queens.

Below is a list of the national and regional retail and fast food chains that I found on a visit yesterday to Jamaica Center.

I first went to this commercial district with my mother to buy shoes back in 1949, which was toward the end of its “Golden Age.” I continued to shop there occasionally for sports equipment and sneakers until I went away to college in 1958. It was not until the early 1980s that I returned to carry out consulting assignments for Regional Plan Association and the Greater Jamaica Development Corporation (GJDC). Though my involvement in the revitalization of this district ended in the early 1990s, I have continued to visit every few years to take photos and gauge its progress. It’s just two miles from my home office.

The revitalization of Jamaica Center has been a long process, starting back around 1968 with the creation of the GJDC. Over a billion dollars have since gone into the revitalization of this commercial center, paying for such things as the re-routing of a subway line (E train), tearing down an elevated line, building York College, the construction of a one million SF Social Security Building, new court buildings, building a terminus for a monorail link to JFK, etc. By the early 19980s the quality of the retailers was ebbing and this trend culminated with the closing of two major department stores, Macy’s and Gertz. White shoppers from the northern and western parts of Jamaica Center’s trade area stopped visiting, choosing instead to drive east to the shopping malls in Nassau County.

Many of the other neighborhoods in the trade area had African American households with relatively high annual incomes for Queens. Cambria Heights, for example, recently had a median household income of $69,030, while the median income for Queens was $49,780. Many of the residents in these neighborhoods were civil service workers and teachers, often in dual income households. Though large numbers of these residents passed through Jamaica Center each weekday to use the subway on their trips to and from work, they, too, avoided shopping there because the retailing had come to focus on low income and teenage markets and the area had developed a reputation for street crime and drug use and sale. Nevertheless, the pedestrian traffic along Jamaica Avenue continued to be a “beehive of activity” and some of the merchants were doing $s/SF that rivaled those of retailers in some of Manhattan’s best locations.

I was greatly encouraged by my recent visit and feel that the end game, the “take off” phase of Jamaica Center’s revitalization is in sight. The primary reason for my optimism is the recent announcement of a major project that will bring over 300 market rate housing units into the downtown, with a number of similar projects on the drawing boards. Another reason is that the retailing’s strength now seems to be more than shops featuring “urban wear,” with chains having a strong middle class appeal opening, e.g., Home Depot, Marshall’s, Zale’s, Nine West, Old Navy. The teens will still shop in Jamaica, but now their parents might as well.

The changing nature of the district’s retailing is also, in my opinion, reflected in the new store facades that have been built in recent years. They are much more attractive, with smaller signage, a better sense of proportion and though the colors used might offend some with Main Street design sensibilities, they are often still very pleasing.

Another indicator of this district’s strength is that commercial rents along Jamaica Avenue recently have reached as high as $150/SF for choice locations.

In the list below I have noted some of the chains that were open in Jamaica Center and have since closed. It should be noted that all of these closures involved chains that were having overall problems.

At the end of the list I have provided a link to a web-based photo album that contains photos of Jamaica Center’s retail chains.

National and Regional Chains in Jamaica Center January 25, 2008

Payless (2 stores)

Gothic Furniture

Quiznos Sub

UPS Store

Java’s Brewin

Game Stop

Burger King

Taco Bell

Pizza Hut

Dunkin Donuts

Subway

McDonald’s (2)

Duane Reade

Walgreens

Sleepy’s

Footlocker Kids (converted to Kids)

Zale’s

Nine West

Radio Shack

Marshall’s

Conway (2)

Home Depot

Fabco Shoes (2)

Footco USA

Jimmy Jazz

Toys ‘R Us (closed, chain in trouble)

Kids ‘R Us (closed, chain in trouble)

Wertheimers (closed, chain in trouble)

Jennifer Convertibles

Rainbow

Ashley Stewart

Tick Tock

Dr Jay’s

Vim

Modells

Cookie’s Department Store

Porta Bella

Strawberry

Parade of Shoes (closed, chain in trouble)

Youngworld

Athlete’s Foot

Shoppers World

Old Navy

The Children’s Place

Gap (closed, chain in trouble)