Here’s a teaser and a link to an article of mine that was recently published in the American Downtown Revitalization Review –The ADRR : How Many Residents Does it Take to Create New Functionally Diverse Downtowns – How to Think About Allocating Scarce Resources to Get There? Adding more housing to our downtowns is likely to be far more complicated than just converting outmoded office buildings, and many of its anticipated positive benefits won’t happen without a proper strategic approach.

The recent strong impact of remote work in our large downtowns on how many office workers show up in their workplaces has sparked calls for the central business districts within them to be made far more multifunctional. Housing, in particular, has been highlighted as the function most in need of buttressing. On one hand the housing is seen as a possible replacement for unwanted office spaces, and a way to save outdated buildings while recapturing lost real estate capital values and rental and tax revenues. However, the main focus in this essay will be on another reason to increase downtown housing offered by advocates of greater downtown multifunctionality: the ability of more housing to improve and strengthen how our downtowns function. The inherent aim is to make our downtowns more magnetic places for people to live, relax, play, and connect. It is an objective consistent with strongly improving the balance between a downtown’s Central Social Functions and its Central Business Functions.[2] When both are strong we have our strongest and most magnetic downtowns.

The owners of downtown office buildings are doing what is economically rational for them to do, to try to regain market share and recapture value. That’s fine, especially since academics are foreseeing a destruction of $413 billion in office values nationally in the near future.[3] Downtown managers and city governments have different objectives. Most importantly, they have responsibilities for the well-being of our entire downtown. They are the ones whose job it is to think strategically and propose needed interventions and incentives that may vary across the geographies of the downtown. Since resources for adding housing are bound to be limited, it is imperative that they have a well-grounded strategy to guide housing growth. Their attention needs to focus on downtown housing in a manner that goes well beyond just the conversion of outmoded office buildings, and to push the interests and concerns of the whole downtown community to the forefront, not just those of troubled property owners. The discussion below covers a number of analytical points and research findings that should help them formulate the needed well-targeted strategies.

An interesting question that currently is getting too little attention is how these two reasons for more downtown housing are related: will the conversion of outmoded downtown office buildings to residential uses necessarily make their surrounding areas better places to live and play? How many new units are needed to significantly lift downtown foot traffic and shopper spending, while reducing visitor fear of crime? Does it make a difference where the new housing is located within a downtown?

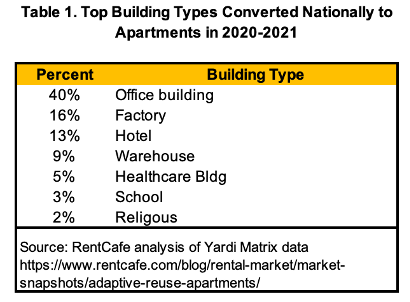

Those critical strategic questions about housing are further complicated by the fact that estimates by real estate experts do not indicate that vast amounts of office space will be converted to residential uses. For Manhattan these estimates range from 8% to about 14% if new regulatory improvements and appropriate financial incentives are added. Furthermore, nationally, most of the buildings recently converted to residential uses were not offices, but had a variety of other uses such as factories, hotels, and even schools and religious – see Table 1. Also, many large downtowns are seeing new housing built in them or on their periphery, and it is often occurring in mixed use multi-building developments, such as Manhattan’s Hudson Yards, and increasingly in new structures that have housing mixed with various combinations of hotel, office, retail, entertainment and personal services spaces, such as the Waterline in downtown Austin. When we think about new housing for our downtowns we need to also think of development paths other than the conversion of outmoded office buildings.

[1] I want to thank Mark Waterhouse for his great editing of this article, and to Paul Levy, Richard Florida, and Andy Manshel for their very helpful comments on an earlier draft.

Here’s the most recent post of The Downtown Curmudgeon vs The Retail Contrarian column Mike Berne and I write for The American Downtown Revitalization Review –The ADRR:

Will Retail Drive The Recoveries In Our Small and Suburban Municipalities?

MJB: So David, last time we went back and forth on the prospects for retail recovery in the more intensely-developed Downtowns of our larger metros. How about, this time, we focus more on suburbs and small municipalities? First, I’d like to give a shout-out to the recently retired Bill Ryan at the University of Wisconsin Extension Center for Community and Economic Development — he and his shop have done such great work over the years on these sorts of Downtowns. Indeed, I’m eager to see what Bill has to say in response to our conversation. O.K., so let’s get to it. Earlier in the pandemic, there was this presumption that many of them would benefit from the rise of hybrid work and the flight from the cities to both suburban as well as second-home communities. Certainly, there have been some high-profile brands — like Starbucks, Chipotle, Sweetgreen, Parachute Home and Faherty — stating explicitly that they would be skewing more towards such opportunities than they had in the past, but speaking more broadly, have you been seeing much evidence of this benefit on the ground?

NDM: Mike, I strongly join your shout out to Bill Ryan at UWEX!! The State should declare him a WI Treasure!

And, of course, I also strongly agree on the small rural and suburban municipalities as our focus in this conversation. As for what I am seeing on the ground, it’s not been much since we have not traveled much outside of NYC since the beginning of the pandemic because of health reasons. That said, I have been looking via the internet into some of these towns I know around the nation and some of their managers and stakeholders, and at the store location functions of the websites of the internet born retailers like Warby Parker and Bonobos, etc. What I am seeing from those sources are that Central Social Functions venues such as food, beverage, entertainment and pamper niche operations – e.g., hair and nail salons, dance and yoga classes –are opening at a faster and larger clip than retail, and that the admittedly small sample of eight or so internet born chains I looked at still are looking at very primo suburban locations, and still not in smaller independent rural cities, in the 25,000 to 75,000 range.

Let me then jump to noting that when we start off by talking about retail chains, we immediately narrow our focus to a much smaller group of downtowns and Main Streets that have any real chance of attracting them. That in turn raises the point that knowing and accepting if your downtown can or cannot attract comparison shopping type retail chains is one of the most important things the leaders in these downtown can do. I know that for me, and I suspect for you, working with these downtown organizations when they have not accepted this reality can be very frustrating. And then even if they can attract chains it will be likely for some kinds and not others.

What I am looking for these days, more than info on the chains, are: 1) if small merchants are really learning how to utilize omnichannel marketing strategies and tools that can enable them to better connect with customers in their traditional trade areas, and to attract e-shoppers from much larger market areas, and 2) the demographic shifts in population, and creatives, to smaller towns and cities, and even some rural areas. While the media and academic focus has been on how the pandemic generates remote workers who may or may not have fled to sparser regions, I think that for retail the far more important trend is that the pandemic really accelerated the adoption and use of omnichannel strategies and tools, and filtered out a great number of operators who were deficient in these skills.

MJB: When I’m presenting on the subject, I always make sure to point out that these expansion-minded DTC’s, along with the still-healthy legacy brands, are only willing to consider a tiny subset of Class A locations. This includes a few suburban Downtowns, though they’re almost always ones that have long been shopping destinations, and in many cases, anchored by an institutionally-owned lifestyle center, like Bethesda, MD (with Bethesda Row) or Walnut Creek, CA (with Broadway Plaza). It is a trend with little to no relevance to 99% of the suburbs and small towns out there.

It is, as you say, all about analyzing and understanding what is and is not realistic for your retail mix. I do think that the Downtowns in these suburban and small municipal settings — which I’ll abbreviate as SSM’s for the purposes of brevity — will be very hard-pressed to support commodity-based businesses which consumers generally patronize on the basis of convenience. Larger cities, with their much higher population densities within walking distance and their much higher tolerance for hassle, have a greater chance of sustaining storefront grocery and drug stores, but in SSM’s, most such tenants — with the exception of Dollar General or a legacy ACE Hardware — will need their on-site parking along high-traffic arterials. In some cases, they might be able to find such opportunities on the Downtown periphery, but more likely, they’ll look to the strip corridor further out, nearer to the freeway interchanges.

A specialty positioning is even more essential in these SSM’s, then. I’m less bearish on the potential for boutiques than most — such shops can and do exist even in the absence of fashion co-tenancy, but only when the merchant is well above-average in sophistication, savvy and resourcefulness. This is also where your comment about omnichannel comes in — it is certainly not a silver bullet but at this point, it is table stakes.

What has struck me — though not entirely surprised me, given how these things generally work — is how so many main streets of smaller towns these days have been adopting the retail forms that originated in and are still primarily associated with the urban core. Driving through Kansas and Wyoming last summer, I saw a lot of them with say, a third-place coffeehouse, a craft brewpub, a denim boutique, a co-working space, maybe a parklet or two. If the community is large enough, there might even be a small-scale food hall. I’d be curious to know how such concepts are received in these places, as I’m not one to believe that what starts in cities necessarily reflects the preferences and sensibilities of every consumer. Then again, there is a Central Social District (CSD) component here that seems universal…

I invite you to sign up for The ADRR’s email edition here . It’s free, and I am sure you will find a range of very interesting content about downtown revitalization presented in a number of appealing formats. The ADRR has taken the lead in covering a number of topics: downtown safety and order; capturing community value; Central Social Functions; the conversion of offices to housing; the impacts of remote work on our downtowns, and retail recovery.

Here’s a teaser and a link to an article of mine that was recently published in the IEDC’s Economic Development Journal. I think its title aptly signals its content.

Let’s Recognize and Leverage the Opportunities the Covid Crisis Has Given Our Downtowns: Some Examples

Abstract

Since the early stages of the Covid19 crisis, our downtowns, especially the larger ones, have been pictured in the media to be either in serious decline or on the verge of failure. While there have been strong analyses that refute such arguments, there has been little recognition of the fact that a robust crisis can not only be destructive and create serious problems, but also new or expanded opportunities for our large downtowns to grow and prosper. These growth opportunities also are appearing robustly in many suburban downtowns. The intent of this article is to attract attention to some of these crisis generated growth opportunities so downtown leaders and stakeholders can start to take meaningful positive active steps to help their districts recover.

Introduction

This article is driven by a deep concern that far too much attention has been paid to doom and gloom prognostications, while far too little is being paid to the opportunities the crisis has created that, if seized upon, can help our downtowns recover robustly.1

While we need to acknowledge that we are not going to have a full return to a pre-Covid world, that does not mean our downtowns are in for a catastrophic future, for it is well known that crises can create substantial opportunities as well as serious challenges. One reason for this failure to look for crisis-generated opportunities is that while the doom and gloom discussions have focused on the Central Business Functions (CBFs) found in our large downtowns, especially office uses, many of these potential opportunities involve venues associated with a downtown’s less appreciated Central Social Functions (CSFs). In turn, that is probably influenced by a widespread misconception that Central Business Districts and downtowns are interchangeable terms.2

Given that for well over 30 years, knowledgeable leaders and admired urbanists such as Jane Jacobs have argued against monofunctional downtowns focused on office work and use, one might suppose that this issue is long settled .3 As Mike Berne, in a recent discussion among downtown experts, stated: “Can someone tell me why the need to convert from sterile, office-only Downtowns to more diversified ones complete with residential is worthy of so many articles these days? Haven’t Downtowns been moving in this direction for a quarter-century now?”4 The answer seems to be that movement away from office monofunctionalism has been very slow, as the current crisis demonstrates, probably because the real estate industry continues to believe the financial highest and best use in these downtowns is office development. That was strongly reflected in NYC a few years ago by the industry’s insistence that the East Side of Midtown Manhattan be rezoned to give a strong priority to very dense office development.

Additionally, while downtown office use may be influenced by strong long term structural challenges posed by remote work and office buildings becoming outmoded because of their inability to attract tenants adopting hybrid work models, the visibility of the recovery and growth opportunities generated by the CSFs is situational, varying with the ebbs and flows of the Covid#19 virus and our ability to cope with it. That means that at first glance these opportunities will often appear to be just potentials, or to lack credibility. However, one might reasonably argue that their persistent resurgence demonstrates a proven strength that will be fully unleashed when either the pandemic significantly ebbs, or we learn how to better cope with it.

Also, the importance of some of these CSF assets, such as housing, attractive public spaces, and strong entertainment/cultural assets, to the health and well-being of our downtowns, and even to the value of their office buildings, too often have not been properly appreciated in the past. In Europe, for example, city centers have not been as dominated by office uses as is the case in the U.S. As downtown office assets have apparently weakened, the spotlight is shifting to these other assets.

The time has come for analysts, leaders, and stakeholders to look at these new opportunities, and to start forging realistic, viable strategies and programs for the recovery and future growth of their downtowns. Moreover, these opportunities may appear in surprising manifestations. An objective of this article is to provide some examples that will encourage downtown leaders and analysts to look for other new crisis generated opportunities in their downtowns.

As many of you may know, the Downtown Curmudgeon is also the founding editor of The American Downtown Revitalization Review –The ADRR. Since almost its inception, members of The ADRR’s advisory board have engaged in an ongoing discussion on a wide range of subjects. A subset of those discussions has been the email give and take between me and Mike Berne, who blogs as The Retail Contrarian. I’d say that we agree about 60% to 70% of the time, but its our interchanges when we disagree that we most enjoy, and from which we often learn most from each other. Recently, we decided that The ADRR would add columnists whose articles would be a regular new feature, and the first of such columns is The Downtown Curmudgeon vs The Retail Contrarian. Here’s the LINK to our first article for that column titled “Whether And How Retail Will Drive The Recoveries In Our Large Downtowns?” Our next column will look at retail in our suburbs and rural communities.

By the way, I invite you to sign up to receive The ADRR’s email edition. It’s free, and I am sure you will find a range of very interesting content about downtown revitalization presented in a number of appealing formats.” The ADRR has taken the lead in covering a number of topics: downtown safety and order; capturing community value; Central Social Functions; the conversion of offices to housing; the impacts of remote work on our downtowns, and keeping our downtowns activated during cold weather.

Throughout the pandemic suburban downtowns have stood out from our largest downtowns in their ability to recover. This was no accident, but the result of the smaller districts not being dominated by monofunctional office clusters, and often actually being far more multifunctional than their larger cousins.

The pandemic has sparked numerous claims that our CBDs (Central Business Districts) are now in decline, and perhaps even perilously so. (1) What is usually lost in such pessimistic analyses is that the areas referred to as CBDs are just large office clusters that are part of the larger downtown. The unexpected and now persistent popularity of remote work, and the consequent empty CBD office spaces certainly lend credence to those claims of weakening. So do the declines in business tourism and a severe thinning of pedestrian traffic on sidewalks usually flush with platoons of office workers at lunchtime and during rush hours.

While all of these deficiencies are undeniable, the assertions that our large downtowns/CBDs are doomed to extreme diminution or death are greatly exaggerated. To understand why our great downtowns are far from doomed we need to properly understand them and their key component parts. Most importantly, they can be not only places where people come to work and make money, but also to socialize and connect with others, to spend money, and to satisfy important personal needs. Moreover, these socially connecting functions are of growing importance to the health and well-being of all of our downtowns. This growth of the socially connecting functions is shifting the nature of our large downtowns. Such a shift would make them much more like our strong suburban downtowns.

Let’s Be Clear About What We Are Talking About

A good starting point is to acknowledge that downtowns are more than geographic areas within our towns and cities filled with clusters of offices and shops. They are complex socio-economic systems, that over time can flex in geographic extent, and the nature and strength of the functions performed within them. To persist and thrive they must change. In the post WWII years, the functions associated with working and making money took physical form in office buildings that dominated our largest downtowns.

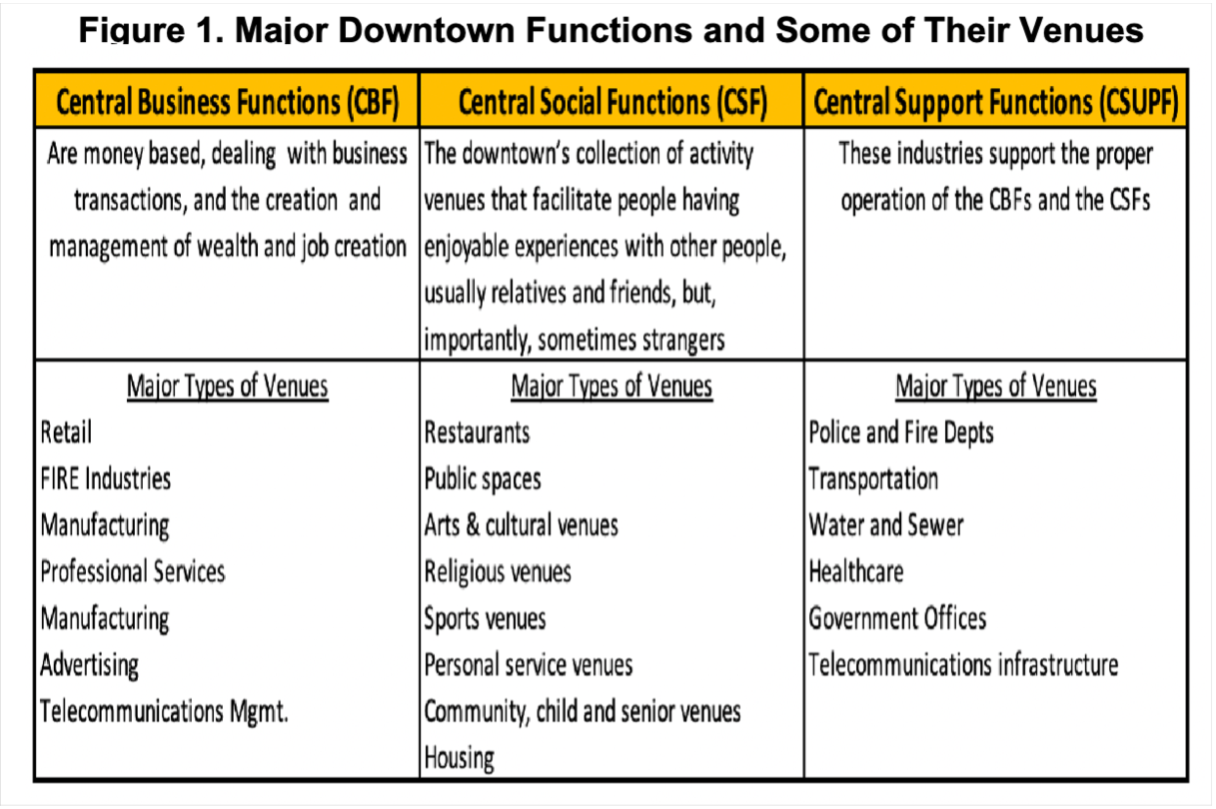

Most of the articles proclaiming that our downtowns are in trouble use the term CBD as a synonym for downtown. This is more than a verbal slight, since it too often leads to a narrow focus on the socio-economic functions associated with office operations, while ignoring or downplaying the other vital downtown functions. Consequently, it is important to consider all of a downtown’s functions, with the most important falling into three categories:

CENTRAL BUSINESS FUNCTIONS (CBFs): These are money based, dealing with work, business transactions, and the creation and management of wealth and job creation

CENTRAL SOCIAL FUNCTIONS (CSFs) : The downtown’s collection of activity venues that facilitate people socially connecting and having enjoyable experiences with other people, usually relatives and friends, but, importantly, sometimes strangers

CENTRAL SUPPORT FUNCTIONS (CSUPFs): These industries support the proper operation of the CBFs and the CSFs.

Figure 1 shows some of the types of venues/operations associated with each group of downtown functions. The CBFs are but one of the three essential functional groups performed in our downtowns, and office operations are but one part of the possible CBFs!

The Ebbs and Flows of Downtown Functions.

Since the Agoras of Greece, the Forums of Rome, and the village wells everywhere in antiquity, places of agglomeration have had Central Business Functions as well as Central Social Functions. Over time the strength and importance of these types of functions have varied. In the late 1970s and 1980s downtowns responded to the post WW II weakening of their CBFs and CSFs caused by the flight to the suburbs of White residents, corporate offices and HQs, and major retailers by building monofunctional office clusters filled with fortress type buildings. This established office buildings as a viable and desirable use in fear ridden times. However, the office centric districts were also deader than door nails most of weekdays — save for rush and lunch hours — and on weekends.

It is notable, that such large office clusters have not developed in the large city centers of Western Europe. Moreover, in the mid 19th Century downtowns in América and Western Europe saw the growth of strong retail functions, especially in the new format of department stores. (See Figure 2). Yet, in recent decades, the viability of department stores in our downtowns has diminished and become increasingly uncertain.

Starting in the late 1990s and accelerating in the 2000s, some of these office centric downtowns, such as Downtown Manhattan and Charlotte’s Center City, turned into much more activated downtowns, drawing local residents, and domestic and international visitors. Sidewalks that had been devoid of people for most of the day then saw platoons of pedestrians even in off-peak hours – see photos in Figure 3.

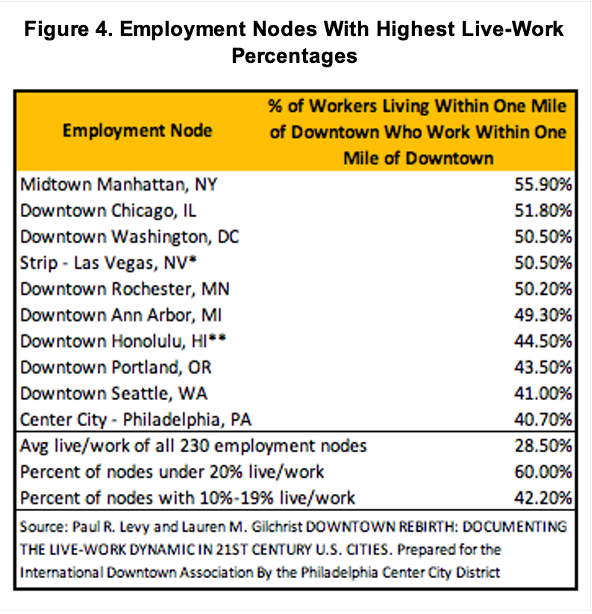

Downtown housing began catching on in the 1990s. New housing units in, but mostly near these downtowns also brought in a pump priming flow of nearby patrons. The number of people who lived and worked in or near a large downtown grew, but there was considerable variation in the degree with which this was achieved. The ten downtowns listed in Figure 4 ranged between 40.7% in Philadelphia and 55.9% in Midtown New York in the number of people who lived within one mile of the downtown who also worked within that area. However, 60% of the 230 employment nodes studied, had under 20% of their residents also working in the area.

There also appears to be an important discrepancy in how much housing actually was going into the downtown core areas versus the more outlying areas of the downtown. Indeed, since these “downtown” residential areas were usually beyond the boundaries of the CBD they were often overlooked in recent discussions of CBD demises. In our largest downtowns offices tended to cluster near commuter rail and subway stations, housing less so. Center City in Philadelphia is having a faster economic recovery from the pandemic than Midtown Manhattan and it is noticeable that Center City’s housing has more strongly penetrated its core area than it has in Midtown Manhattan. During the crisis residents still went out for necessaries and pedestrian traffic and retail sales have done much better in downtown residential areas than in their office clusters.

Large downtowns with insignificant housing in the core seem to be those struggling the most to bring workers and pedestrian traffic back to pre-crisis levels.

While the need for our large downtowns to become more multi-functional has been recognized by some for several decades, the recent pandemic has revealed that many have not done so, especially in their core areas.

Learning From Suburban Downtowns. While employment center functions have long dominated our major downtowns, this has been far less the case in our suburban and independent rural cities. Their downtowns are seldom referred to as CBDs, because their CBFs are seldom dominated by a large office cluster. Yes, they often can have a relatively significant number of people working in them, but they seldom are the location for most of the people working in the town. As can be seen in Figure 5, in the cities with the most jobs – Dublin, Downers Grove, La Crosse and Appleton – their downtown areas only hold between 3% and 7% of them.

And yes, these suburban downtowns can have a significant number of office spaces, though they usually are neither in high rise buildings nor in a dense cluster. Many are scattered among second story and some storefront spaces. Given that the people who work in these towns commute overwhelmingly by auto, offices have not been prime drivers of TOD in these downtowns. That role has usually been played by housing.

Morristown is a very interesting town because it has long been a standout as a unique suburban downtown employment center, that even these days has about 43% of the city’s jobs. Yet years ago, its political and business leaders worried about its well-being because the offices alone where not taking the district where they wanted it to go. Today, the downtown is vibrant, well activated, with a slew of CSF venues and places such as a PAC that draws 200,000 people annually, The Morriston Green public space, about 100 eateries and watering holes that average over $1 million/yr in sales, and a very strong pamper niche adding much to its magnetism. It has just a few national retail chains, but many successful small boutiques. It is widely acknowledged that what turned this downtown around was not its offices or retail, but the 1,500 or so new residential units that were built between about 2000 and 2010, with more units added consistently since then. This pattern of new downtown housing sparking the development and growth of CSF venues is replicated in a growing number of affluent suburban downtowns across the nation. Cranford, NJ, for example, has built 366 Transit Oriented Development housing units since 2006 – see Figure 6 – boosting the vibrancy of Its CSF venues. Out in the Midwest, take a ride on a Metra train from downtown Chicago to Aurora and one finds town after town with lots of residential units near their rail stations.

An important lesson our large downtowns can learn from these successfully urbanized suburban downtowns is that strong, dominant CBFs are not required for a downtown to be strong and successful if it has strong CSFs!

Another important lesson is that housing near rail stations that are located in the downtown core may be a very sound idea. That would be in sharp contrast, for instance, with:

The current situation in Midtown Manhattan where the residential units within this downtown are overwhelmingly at its edges and not its core

The State’s current plan in NYC to raze the area around Penn Station between Sixth and Ninth Avenues from 30th to 34th Streets, and fill those properties with very large office buildings. (2)

Also, it may be a very sound idea for office spaces in our largest downtowns not to be part of any substantially sized office building cluster, but as parts of either clusters of mixed use buildings or mixed-use clusters of buildings specializing in different functions. One way or another, however, it is essential that substantial housing be brought into the core office area. Happily, projects of this kind are happening. The rehabilitation of the 40 story Seneca One Tower in downtown Buffalo, NY is a great example of what such a mixed use building might contain. It combines 115 apartments, with office spaces, a food hall, a large gym and a craft brewery.(3) In downtown Dallas the 50-story Thanksgiving Tower is undergoing a similar mixed-use transformation that will have a substantial number of residential units. In Lower Manhattan’s financial district, the conversion of One Wall Street from office to residential uses will provide over 500 units and be the largest such conversion in the city’s history.

The opportunities for such large conversions of existing office spaces may be relatively hard to find, but when they occur their impacts on a downtown can be substantial in terms of generating non office worker foot traffic and the businesses to serve it.

The problem with converting most large modern office buildings to residential uses is reportedly their large floor plates with most space distant from windows. So far, the mixed use conversions have the offices still occupying these large floors, while the conversion to housing occur on smaller and usually higher floors. One might wonder if some property owner might try a mixed use program on the larger floors, with spaces along the windowed perimeter taking on residential uses, and the remaining window-distant spaces retaining their office uses?

Affluent CSF Driven Suburban Downtowns Will Recover Quickly and Strongly from the Crisis.

Morristown and many other wealthy suburban downtowns are also primed for recovery because they suffered far less from the Covid crisis than have their big city cousins:

They were much more dependent on residents than office workers or domestic and international tourists than most of our large downtowns

They have lots of new housing units within their downtown cores, often within a 10 minute walk of their commuter rail station.

Their restaurants and other CSF venues were and are bringing people downtown

Their pedestrian traffic returned much quicker than it has in our large downtowns

Any tourist flows, are overwhelmingly domestic, and are returning quickly.

In addition, the crisis has positively impacted on their assets:

It has significantly increased the number of residents who work remotely and are now part of the downtown’s important daytime population. Conversations with several suburban downtown managers found that merchants definitely have noted their presence.

It has accelerated a trend that was already apparent prior to the crisis of Millennials in search of affordable housing and good schools moving from their region’s central city greater downtown areas to the suburbs. Unfortunately, this trend also has a downside – rising housing costs.

Metuchen, NJ is another downtown positioned for a quick recovery and demonstrates many of their characteristics. It started a major revitalization effort in 2016 and since then has seen about a $169 million invested in the downtown, with 397 new residential units being built. Many of these units are near the commuter rail station that has direct connections to New York, Newark, and Trenton.

Metuchen’s residents have high median household incomes $128,619 and 62.5% have a BA degree or higher.

Between March of 2020 and March 2021, 33 downtown businesses closed, while 38 opened. Interestingly, 55% of the new businesses were related to CSFs—they are already leading the way to recovery. Here again, these downtowns provide a useful lesson for our larger downtowns.